while we were watching

a page on what i found when i stopped looking at the rocket. 8 min.

coffee's hot.

the world's still waking up.

come sit.

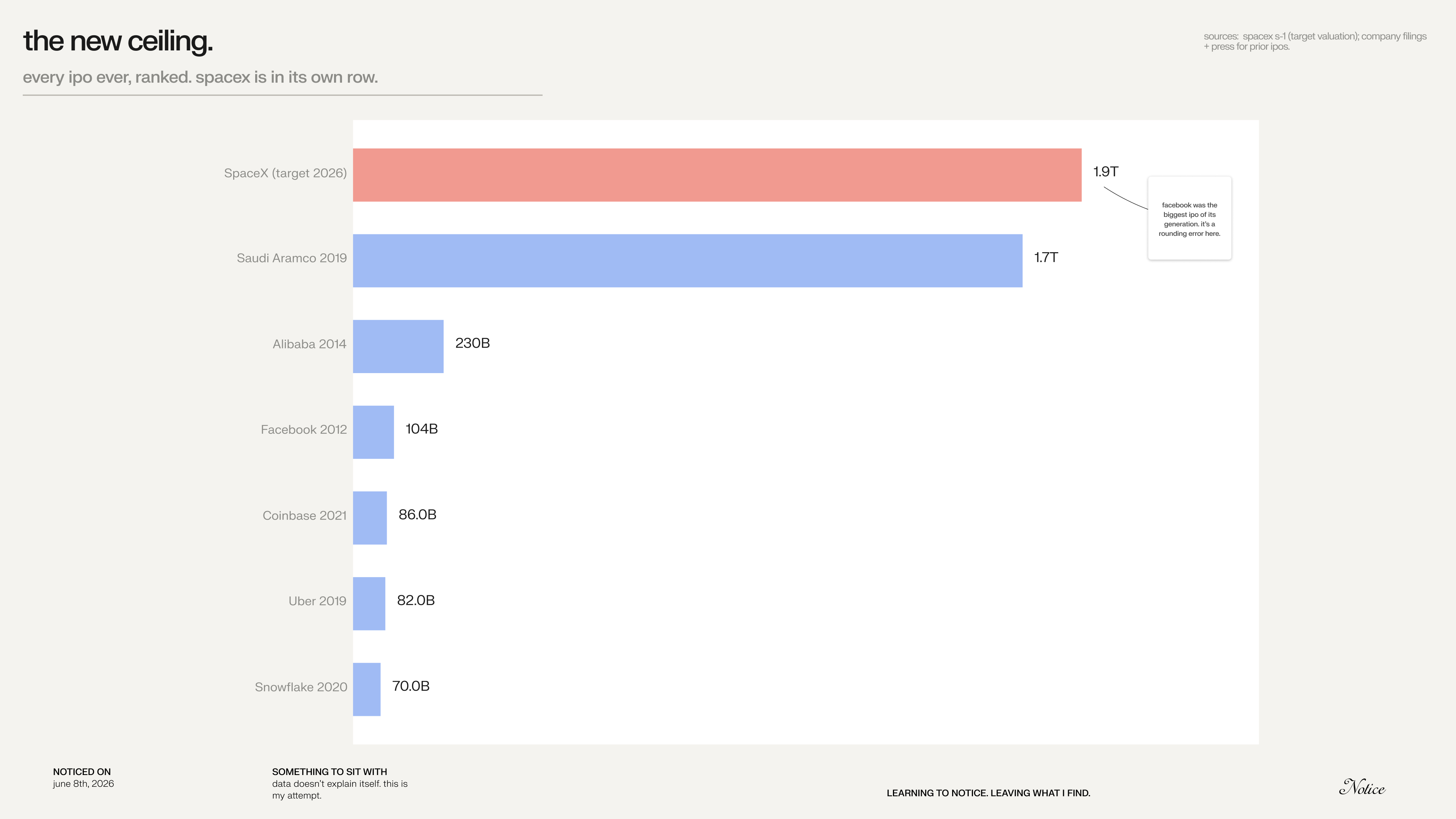

spacex is about to be the biggest ipo that has ever happened.

a target around 1.9T. bigger than facebook. bigger than alibaba. bigger than aramco.

that’s interesting.

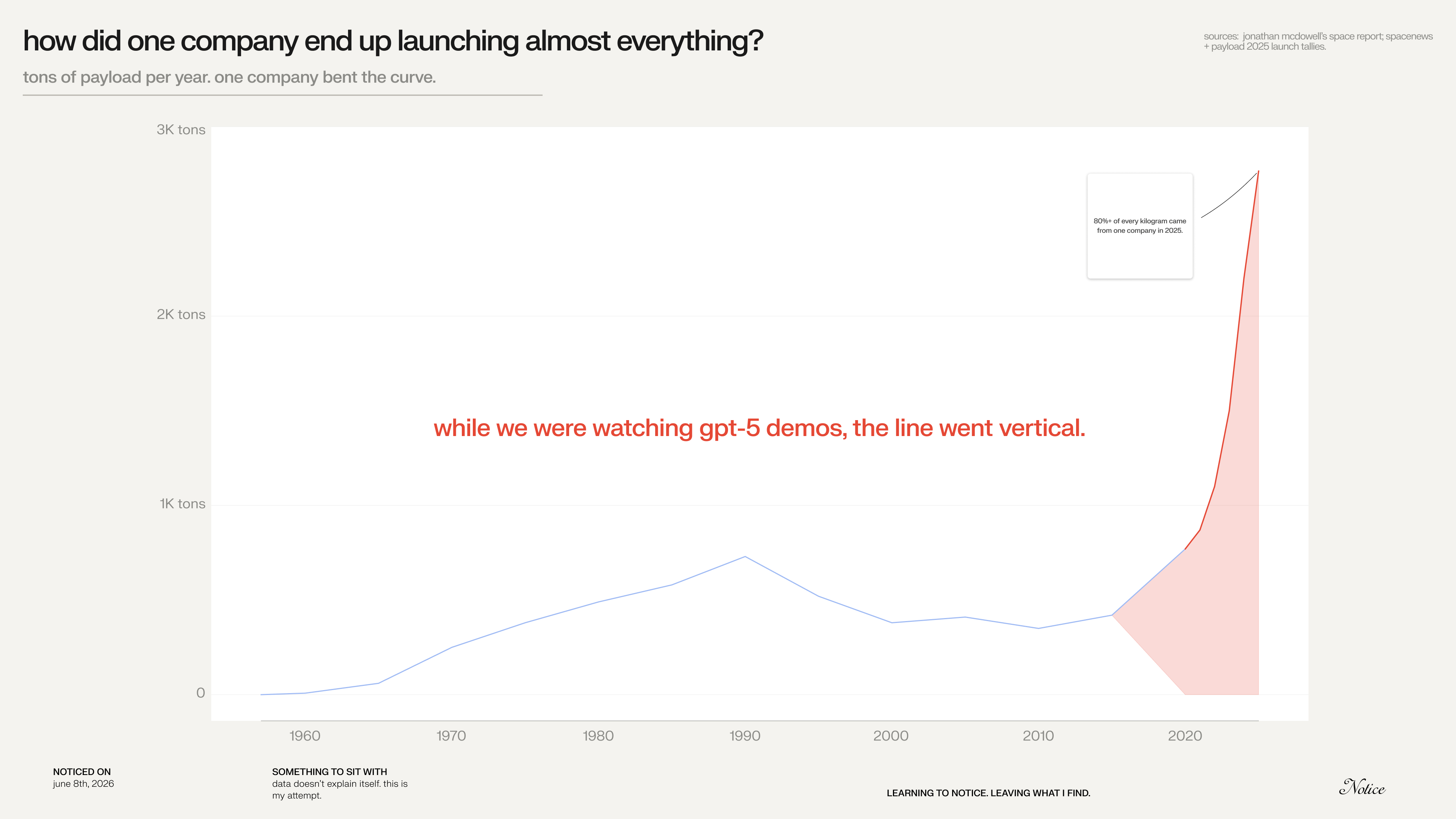

this is more interesting.

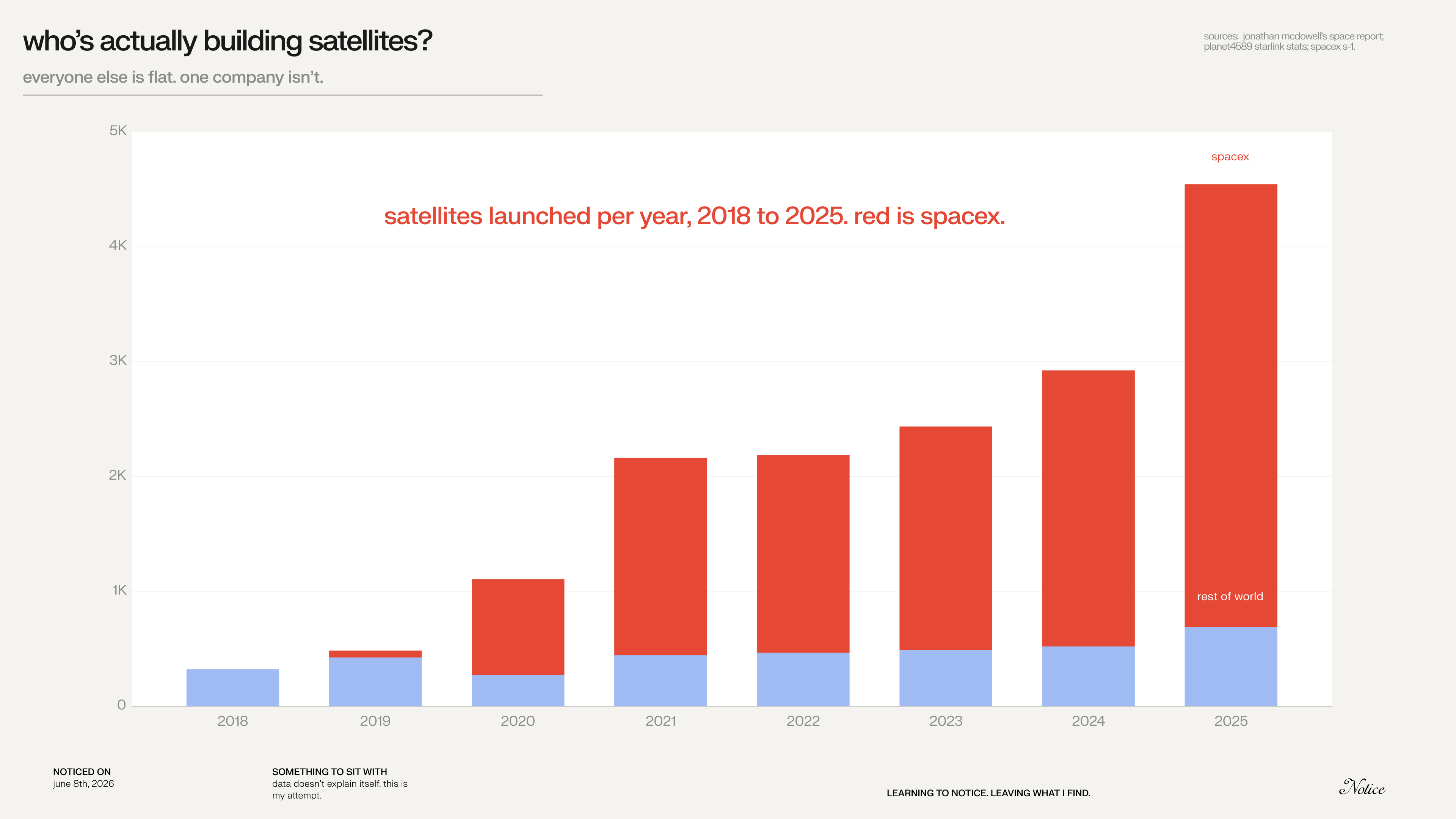

look at the red part. 2020 to 2025. 70 years of human space history, and the last five took the whole curve and bent it.

spacex flew 165 falcon 9 missions in 2025, more than the rest of the world combined, and the dominant share of all mass to orbit per jonathan mcdowell’s tracker.

while we were watching the gpt-5 demos, that happened.

and once i saw it, the rest of the s-1 started reading differently.

what is actually happening.

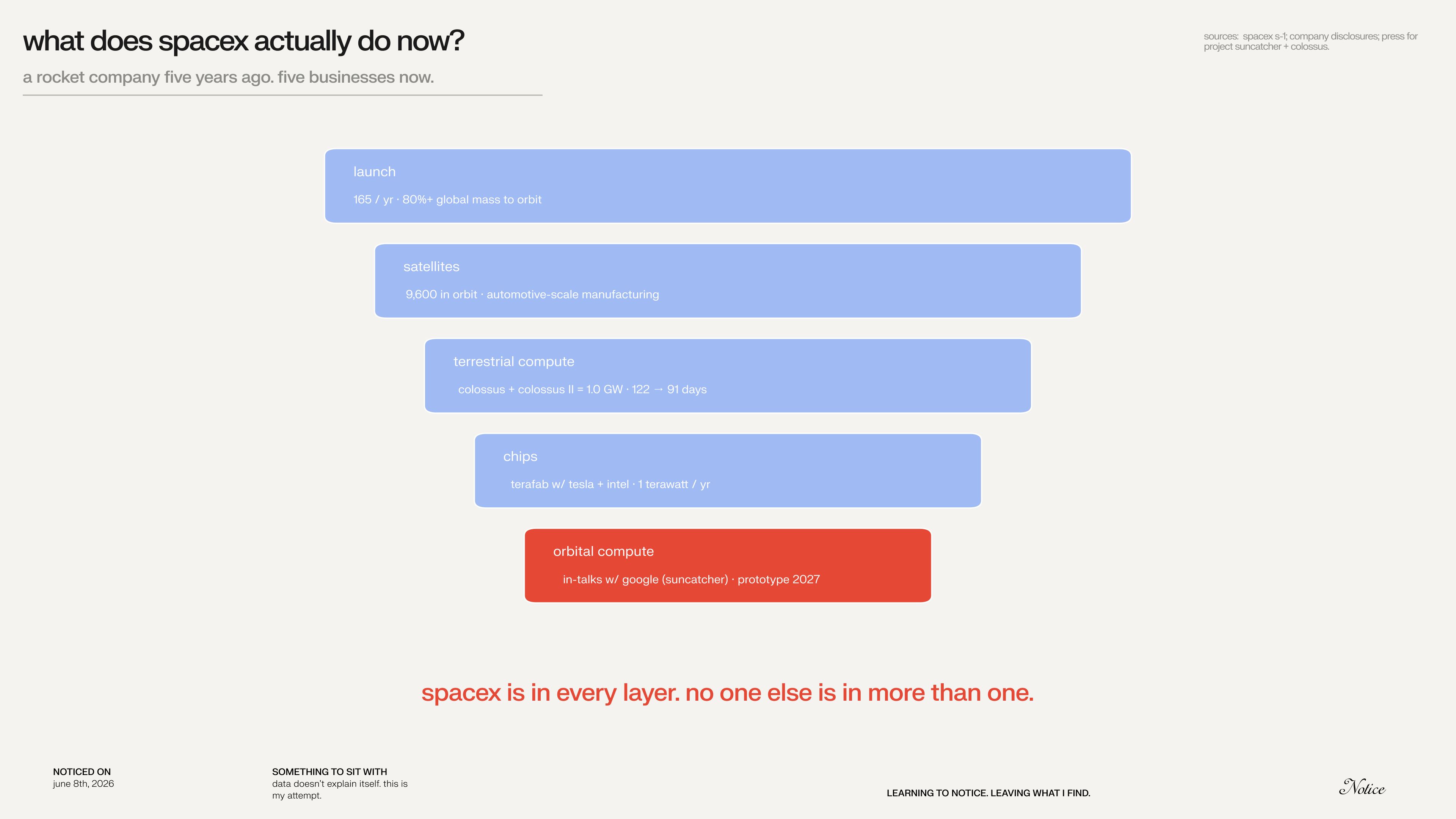

so what is spacex now, actually? because it’s not just a rocket company anymore.

first they learned how to move things. then they learned how to build things. now they’re learning how to power and compute things.

that’s the shape. five layers. they’re in every one.

move things (launch). a falcon 9 has two parts that matter. the booster (the big bottom that pushes everything off the ground) and the second stage (the smaller one that takes the payload the rest of the way up). spacex figured out how to catch the booster, refurbish it, fly it again. the rest of the world is still throwing theirs away. that’s how one company ended up doing 80% of the mass. and most of that mass is their own. starlink launching starlink. that’s not a launch business winning a market. that’s a manufacturing machine feeding itself.

build things (satellites). they don’t make satellites the way satellites used to be made. they make them on a line. nearly 10,000 starlinks in orbit, per jonathan mcdowell’s tracker. that’s not a space program. that’s an automotive factory pointed at the sky.

power things (terrestrial compute). somewhere along the way, the rocket company started pouring concrete. colossus + colossus II = 1.0 gw of compute online in memphis. yes, really. (this is also the xai side of the house. the two merged in feb 2026. spacex didn’t build the ai layer. it bought it. but the manufacturing logic is what makes the purchase make sense: you don’t buy a compute business, you buy a factory you already know how to run.)

silicon. most people see ai and think software. eventually every ai story becomes a factory story. that was the whole point of last week’s syllabus. the s-1 names a thing called terafab. a “chip manufacturing initiative with tesla and intel” whose long-term goal is one terawatt of compute hardware per year. that’s the biggest leap in the whole stack. tesla and intel making a terawatt of chips a year is a stated ambition, not a fab that exists, and it’s the line i’d bet against soonest. but even as an ambition it tells you what the company thinks it is: no longer a launch business. and from the same filing, a quieter line that load-bears the whole stack: “the future of ai will be determined by the control of the physical stack.”

compute in space (orbital). google announced project suncatcher in november 2025. solar-powered tpu constellations in low earth orbit. planet labs builds the satellites; google is reportedly in talks with spacex for the launches. prototype mission slated for early 2027. this is the bet at the top of the stack. solar-powered compute that doesn’t need a grid or a cooling tower, because space already is one. this is where last week’s syllabus on the physical layer beneath the ai story and gavin baker’s framing land: cities are already banning new data centers, so the next ones have to leave the planet.

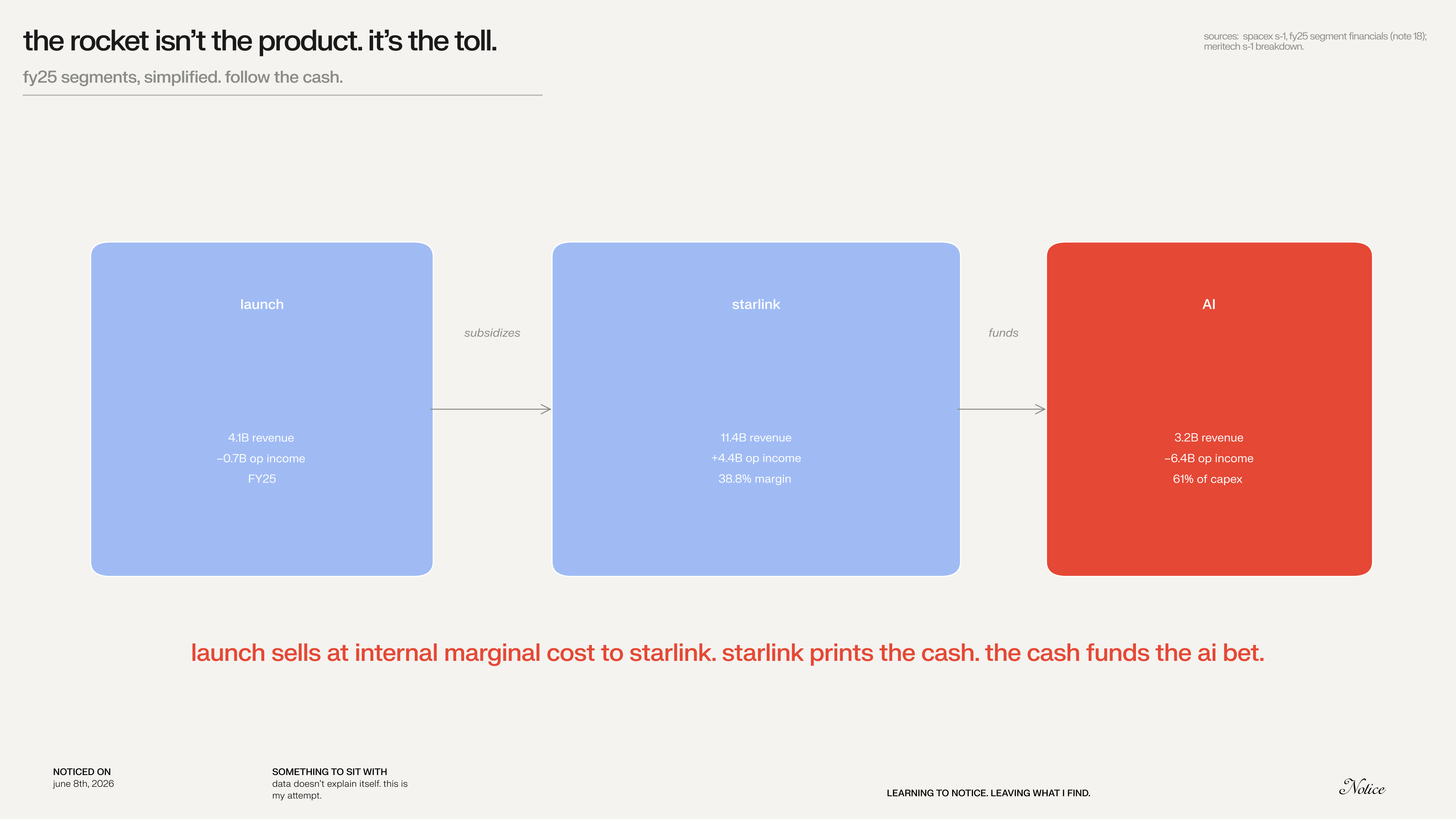

okay but how does this all hang together financially?

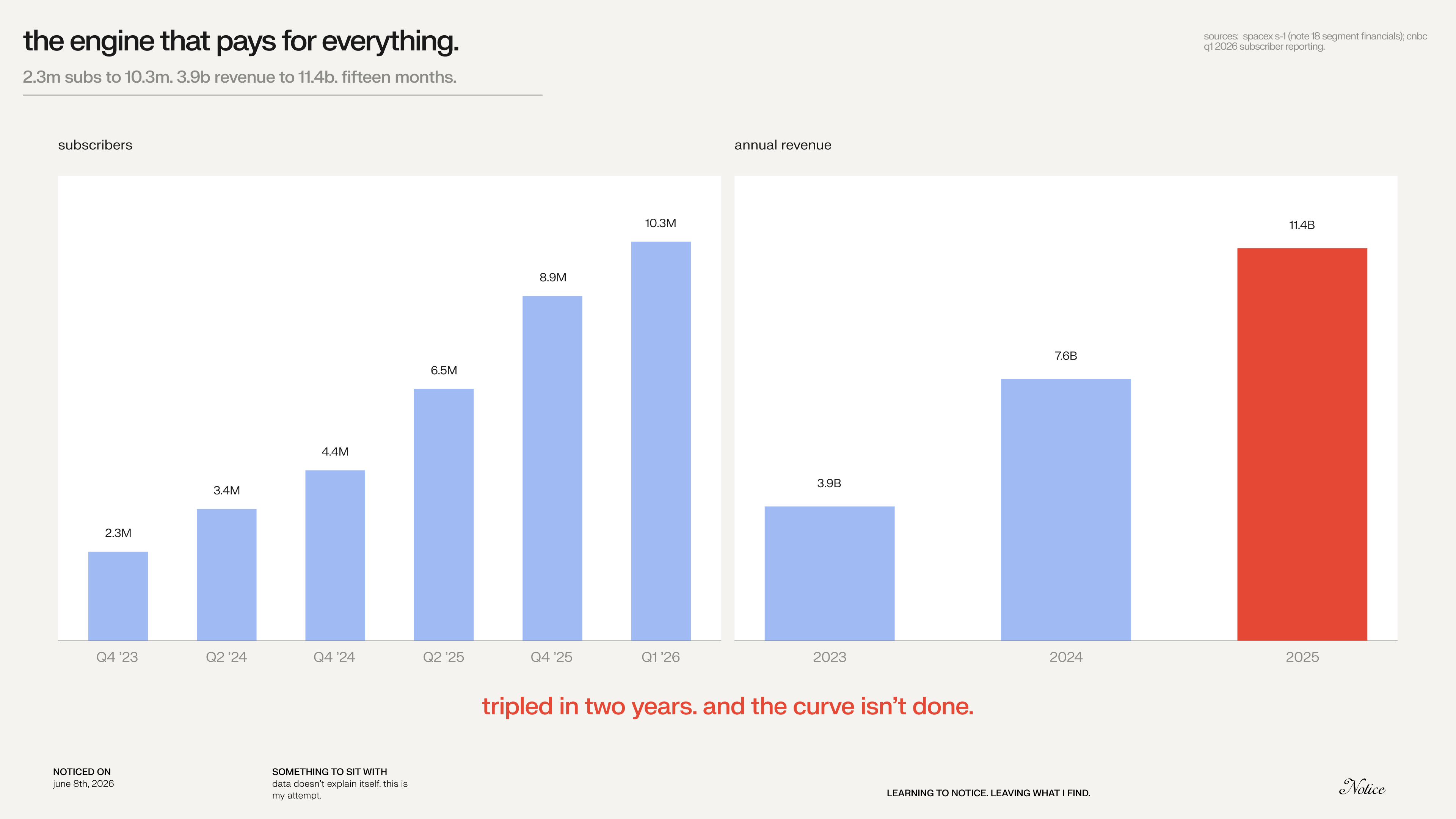

launch sells at internal marginal cost to starlink. starlink prints the cash. 11.4B in revenue in 2025, 49.8% year-over-year growth, and roughly 38.8% segment margins per the s-1. the cash funds the ai bet (which lost billions and ate the majority of capex).

that’s the architecture. spacex is a vertical manufacturing loop that uses launch as a cheap toll booth. the rocket isn’t the product. it’s the toll. and every dollar it collects gets reinvested up the stack.

what i noticed.

once you see the stack, you start noticing things in the s-1 that didn’t make sense before.

this week i kept staring at three numbers. they’re all the same number, really. they all say spacex is a manufacturing system pretending to be other things.

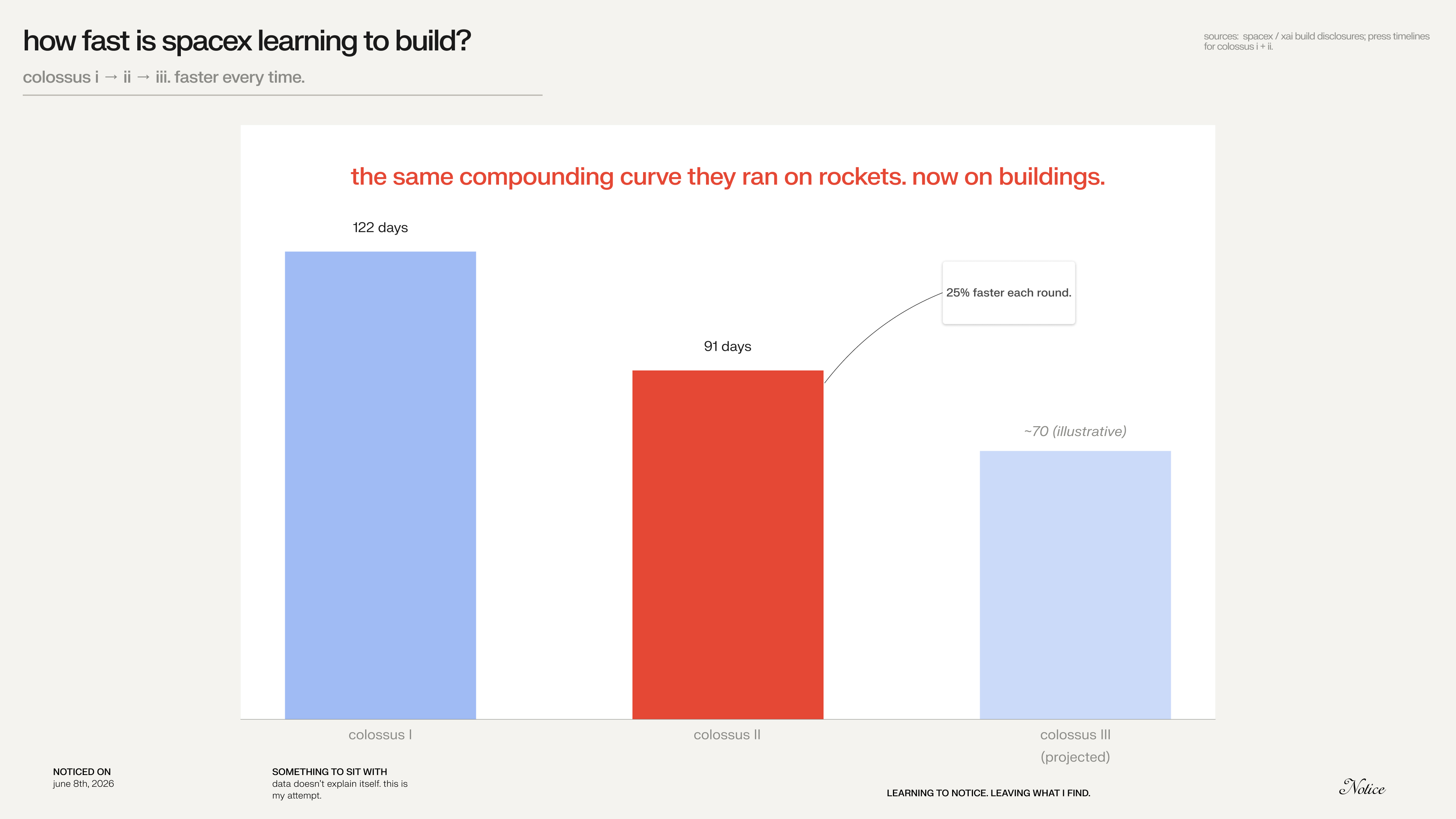

fingerprint one. colossus.

colossus I took 122 days to build. colossus II took 91. that's 25% faster, build over build. the same compounding curve they ran on falcon 9 boosters, now on data centers. the company that learned how to shorten rocket cycles is shortening building cycles.

fingerprint two. the wedge.

look at how flat the rest of the world is. then look at the red. spacex deployed 3,180 starlinks in 2025 alone. more than the rest of the world combined. while everyone's debating chip allocation, spacex turned a satellite line into a car factory. the wedge is a manufacturing curve, not a launch curve.

fingerprint three. the cash engine.

starlink subs more than doubled in 2025, from 4.4M to 8.9M, and hit 10.3M by end of q1 2026. revenue tripled in two years: 3.9B → 7.6B → 11.4B, still growing 49.8% at 11B scale. that doesn’t happen at this run-rate very often. this is what shortening production cycles does to economics. cost falls. base widens. cash compounds. the curve isn’t done.

every one of these is the rocket logic applied somewhere else. the rocket was practice.

how i’m seeing it.

so what do you actually do with this. here’s how i’m seeing it.

one sentence that holds the whole thing together: the thing that could break in the next twelve months is the thing that compounds for thirty years if it doesn’t.

let me show you both sides.

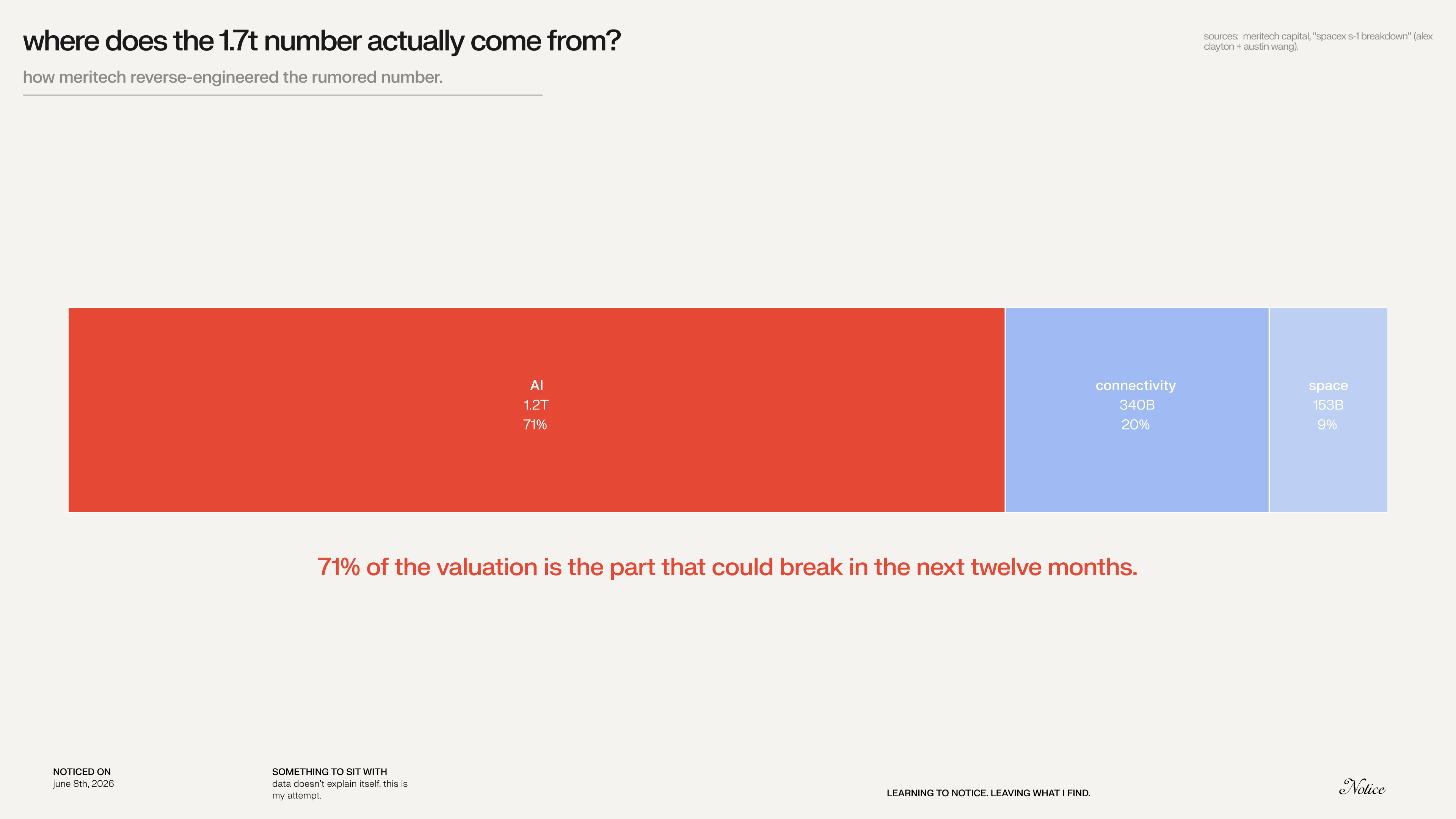

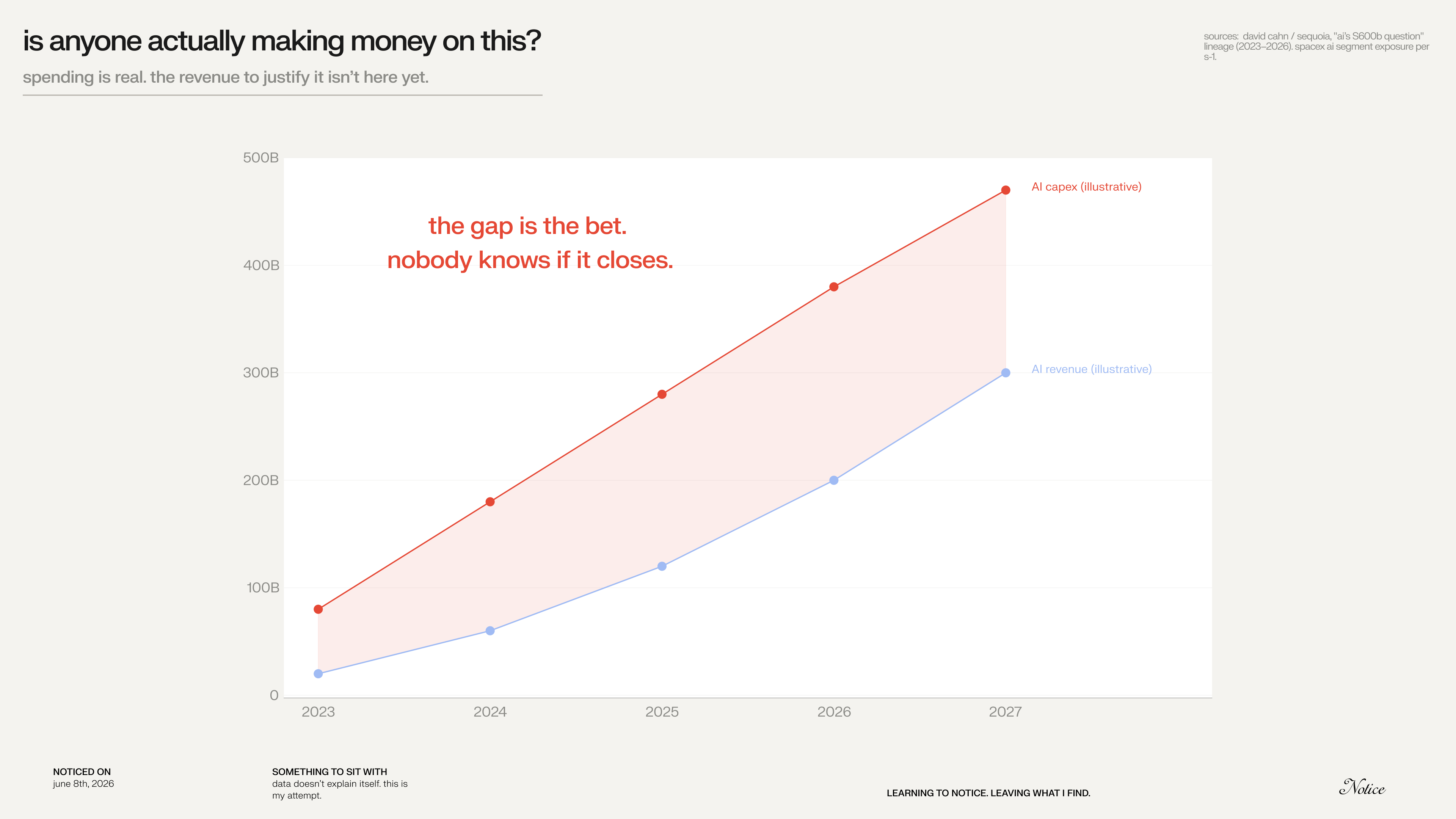

the break. 71% of the valuation sits on a segment that lost 6.4B last year.

meritech’s s-1 breakdown (by alex clayton + austin wang) backs into the rumored 1.7T number, and ai does 71% of the work to get there. they’re explicit: they’re not justifying the number, they’re showing what it takes. most of the company sits on the segment that lost the most money. that could go in twelve months if ai demand softens or chip allocation pulls back.

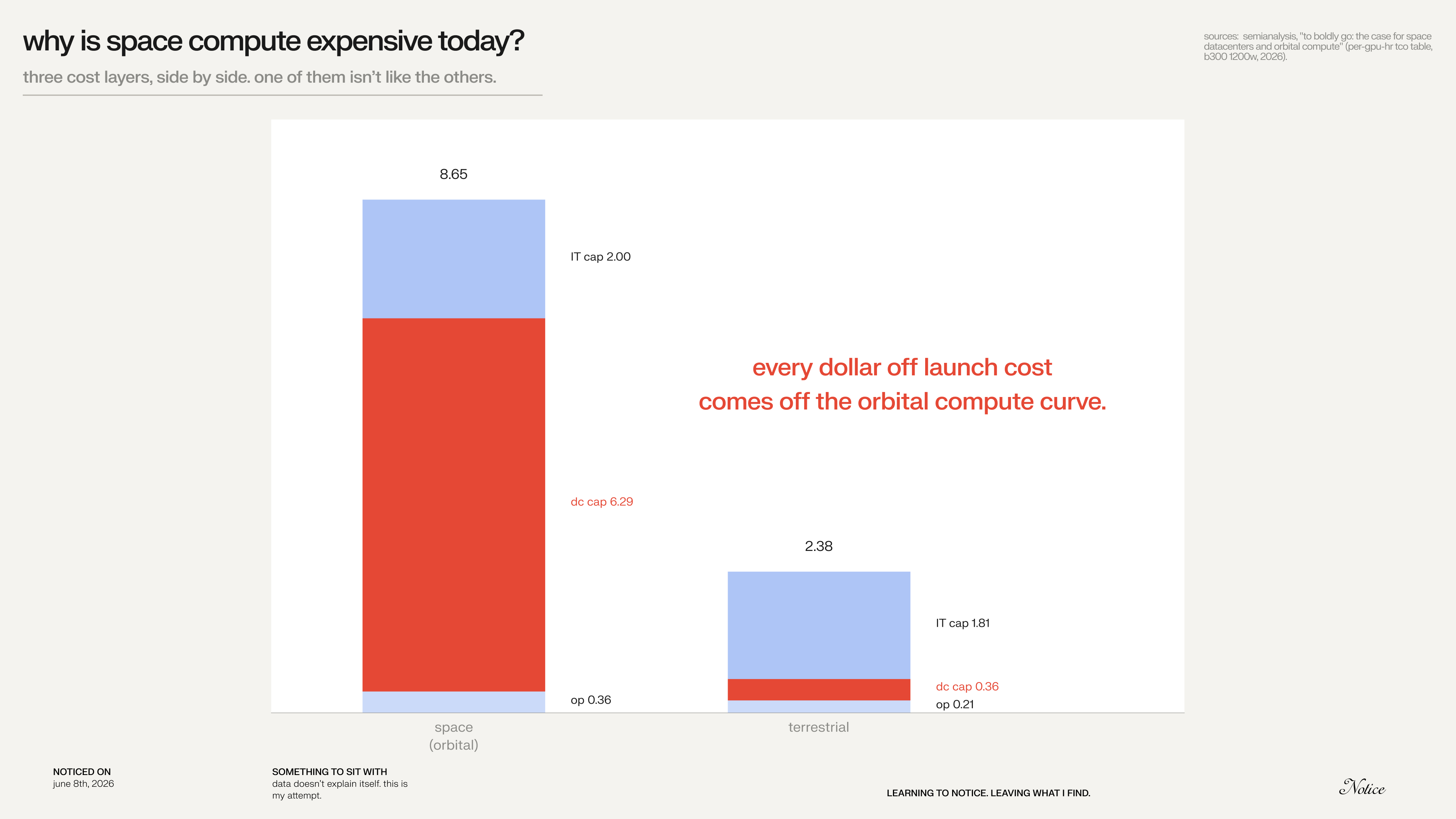

the compound. semianalysis broke down what the cost stack actually looks like today. space datacenter compute: $8.64 per gpu-hour. terrestrial: $2.37. that’s a 3.6x premium.

the gap isn’t engineering. it isn’t power. it isn’t operating cost. it’s mostly one line. datacenter capital cost. $6.29 vs $0.36 per gpu-hour. that’s launches.

which means the cost curve mostly tracks one variable: what falcon and starship cost per kilogram to orbit. cooling, radiation, and replacement cycles aren’t free up there either, but launch dominates the gap and it’s the one falling fastest. every dollar off launch comes off the orbital compute curve. it’s one model, not a law. parity around 2035 in the musk scenario, 2039 in the semianalysis base case. either way the bear case is already a ramp. the direction is the part i’d bet on.

the shift in between.

which raises the next question: does the ai bet actually pencil? if it does, the whole loop runs. if it doesn’t, the toll booth is still a toll booth. just less interesting.

the honest answer: not yet, and not for a while. and here’s the part that keeps me patient about that. the binding constraint right now isn’t power. it’s chips. semianalysis calls it the great ai silicon shortage. ai demand eats roughly 60% of tsmc’s leading-edge output in 2026, around 86% in 2027. and that constraint is universal: it doesn’t care whether the datacenter is in memphis or in orbit. space doesn’t solve the chip problem. it solves the power problem. but only in the world where ai demand is so enormous it’s blown past everything we can build on the ground. that’s why this is a thirty-year bet, not a twelve-month one. it’s also why terafab exists: the only way to beat a chip constraint is to make more chips.

the 30-year thesis in one line: launch costs commoditize → spacex owns the cheapest path to orbit → orbital infrastructure becomes a real market. everything else is texture.

some lingering thoughts.

and here’s what would make me change my mind. not as disclaimer. as a dashboard.

the worst thing i could do is fall in love with the story. so here’s what i keep turning over.

the ai buildout’s capex still hasn’t shown up in revenue. david cahn at sequoia has tracked the gap since 2023. 125B, then 600B, then trillions. it widens every update.

if the labs never print fast enough and the whole stack reprices, who’s left holding spacex’s ai segment when it reprices too?

then the rest of what i keep turning over:

starship is the load-bearing assumption under the entire cost curve. three of the last eight tests were ruds. rapid unscheduled disassembly, what spacex calls “it blew up.” they’re learning fast. but what if fast still isn’t fast enough, and rapid reuse slips three years? does the whole orbital thesis just sit and wait?

colossus went from 122 days to 91. but what if that pace was memphis. just the water, the power, the permits lining up. not a repeatable machine? how much of the manufacturing fingerprint is the company, and how much is one good location?

and the one that’s really been on my mind:

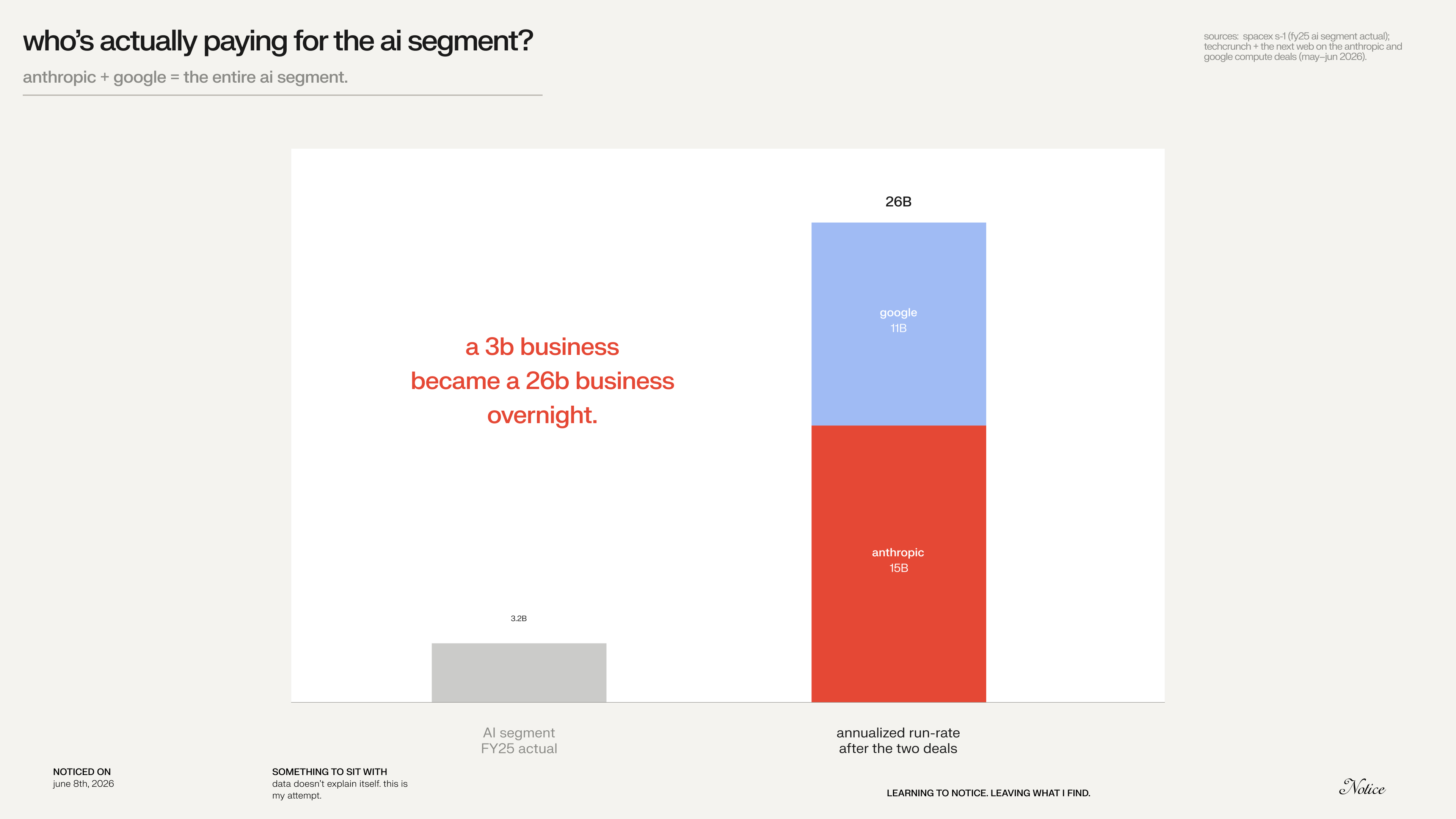

the entire ai segment is two rental contracts. and it carries 71% of the valuation. anthropic pays 1.25B/month for the whole output of colossus 1. then three days ago, google signed too. 920M/month for gemini enterprise. ~26B a year, combined. (yes, the same google that’s in talks to launch suncatcher. it shows up on both ends of the stack now.)

two of the best-funded companies on earth. that sounds like diversification. it isn’t. both leases end in 2029. both tenants are ai labs. which means both are exposed to the exact capex vs revenue gap from the chart above. if that gap forces a reprice, it doesn’t take one customer. it takes the whole segment, at the same time. so what is the ai segment actually worth if both leases come up for renewal into a market that’s decided ai compute was overbuilt?

if all of it breaks at once, the rocket is still cheap. it just stops being the factory equipment for anything bigger. still a launch monopoly. just not 1.9T.

i don’t know which way it goes. nobody does. but i know what i’m watching, and i know what would change my mind.

what i’m sitting with this week: i thought i was looking at a rocket company. i was actually looking at a manufacturing machine that kept expanding into adjacent layers. that reframe is the only thing that made the s-1 stop feeling weird.

if launch costs commoditize the way semianalysis thinks they will, who owns the orbit?

— brylan.