the price of belief

a page on tesla. sit with it. 8 min.

what’s playing: late night thinking session — mikecol, quasar, lion babe, gold link.

spent my birthday in orlando with my mom and sister. we watched the spacex rocket launch. i don’t have words for it yet. just that i’ll never forget it.

got back to chicago. the lake was frozen solid. something about seeing it from the plane. still, quiet, holding everything underneath.

then there was the tesla earnings call. elon mentioned terafab. robotaxi. amazing abundance. the stock’s at four eighteen. watching something take off is one thing. evaluating whether this one will is another.

and dating. i spent time with two women since i landed.

dinner wednesday night. she’s been showing up differently. on time. asking questions. transparent about where she stands. the hug after felt different. the three-hour facetime felt like home. but i’ve been here before. i know how this can go. so i’m paying attention. skeptical but open. wanting to believe, but needing to see it first.

then friday night. electric. we caught a vibe. but the signs were there. small comments, inconsiderate moments, things that didn’t add up. i noticed. didn’t act. by the end of the night it came out sharper than it should have. we won’t see each other again. she’s not wrong for how she moves. she’s just not my person. i don’t need to teach reciprocity. i just need to notice faster and leave earlier.

same week. one where the change might be real. one where i knew better and stayed anyway.

so what does this have to do with tesla?

how this kind of business works.

tesla makes money three ways today:

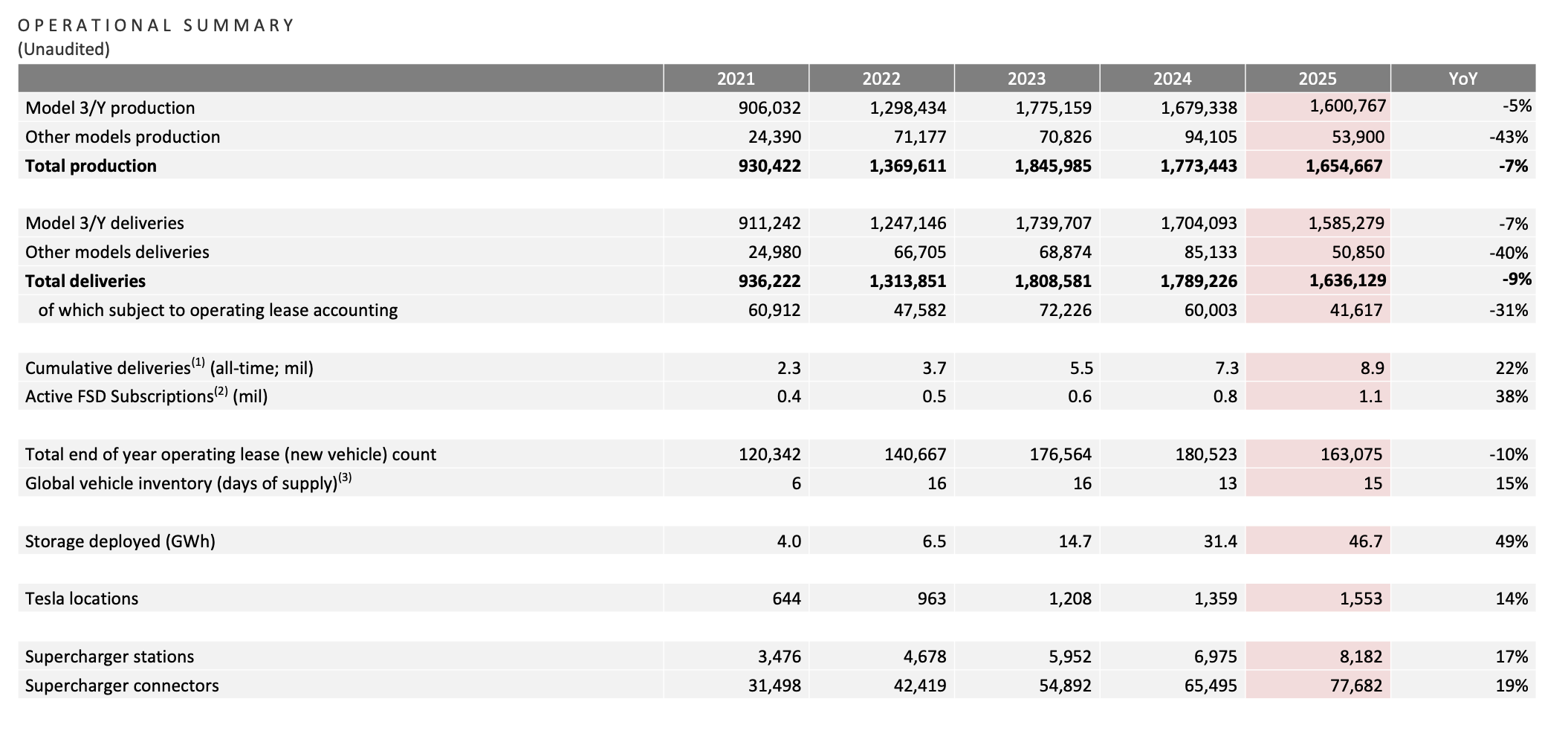

cars. about seventy billion in revenue, but shrinking. down ten percent last year.

energy. nearly thirteen billion, almost doubled in two years. backlog strong.

services. supercharging, insurance, parts. another twelve and a half billion.

but the interesting part isn’t where the money comes from. it’s how the pieces connect.

they own the stack. cars generate data. data trains the software. software enables autonomy. autonomy unlocks robotaxi. robotaxi funds the next thing. energy powers all of it.

the third thing isn’t a business yet. it’s the bet.

robotaxi. optimus. physical ai. if it works, they’re not selling cars or batteries. they’re selling labor hours and transport miles. think airbnb for cars. you let your tesla work while you sleep. recurring revenue at software margins on physical infrastructure they already own.

they just sunset the upfront fsd purchase. subscription only now. that’s a signal. they want recurring revenue, not one-time payments. the business model is evolving.

and now they’re going deeper.

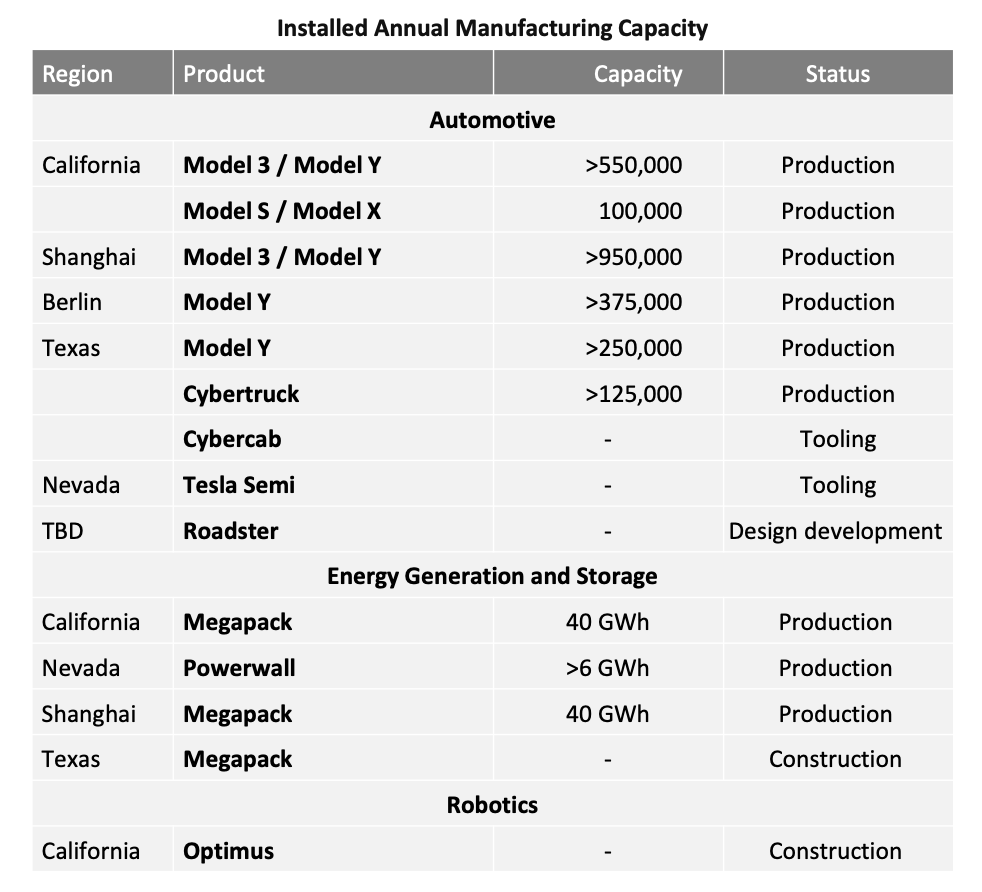

elon announced a “terafab” on the earnings call. a us-based chip factory for logic, memory, and packaging. he’s spending his saturdays on the ai5 chip design. they’re building lithium refineries and cathode facilities. they want to make their own solar cells.

model s and x are being discontinued. fremont is becoming an optimus factory. one million humanoid robots a year is the target.

the mission got updated. tesla is now chasing “amazing abundance.”

they’re not asking you to see them as a car company anymore. they’re asking you to see them as infrastructure.

the story being told.

every few years the story shifts. electric vehicles. full self-driving. robotaxi. optimus. each time the current thing gets challenged, a new future thing justifies the valuation.

that pattern makes me cautious. it’s like watching someone promise they’ve changed, then promise again, then promise again.

but here’s what’s different this time. it’s not just narrative.

gross profit held despite revenue decline. they’re doing something on the cost side. r&d spiked sixty percent. they’re putting money where the words are. and they have the balance sheet to fund this themselves.

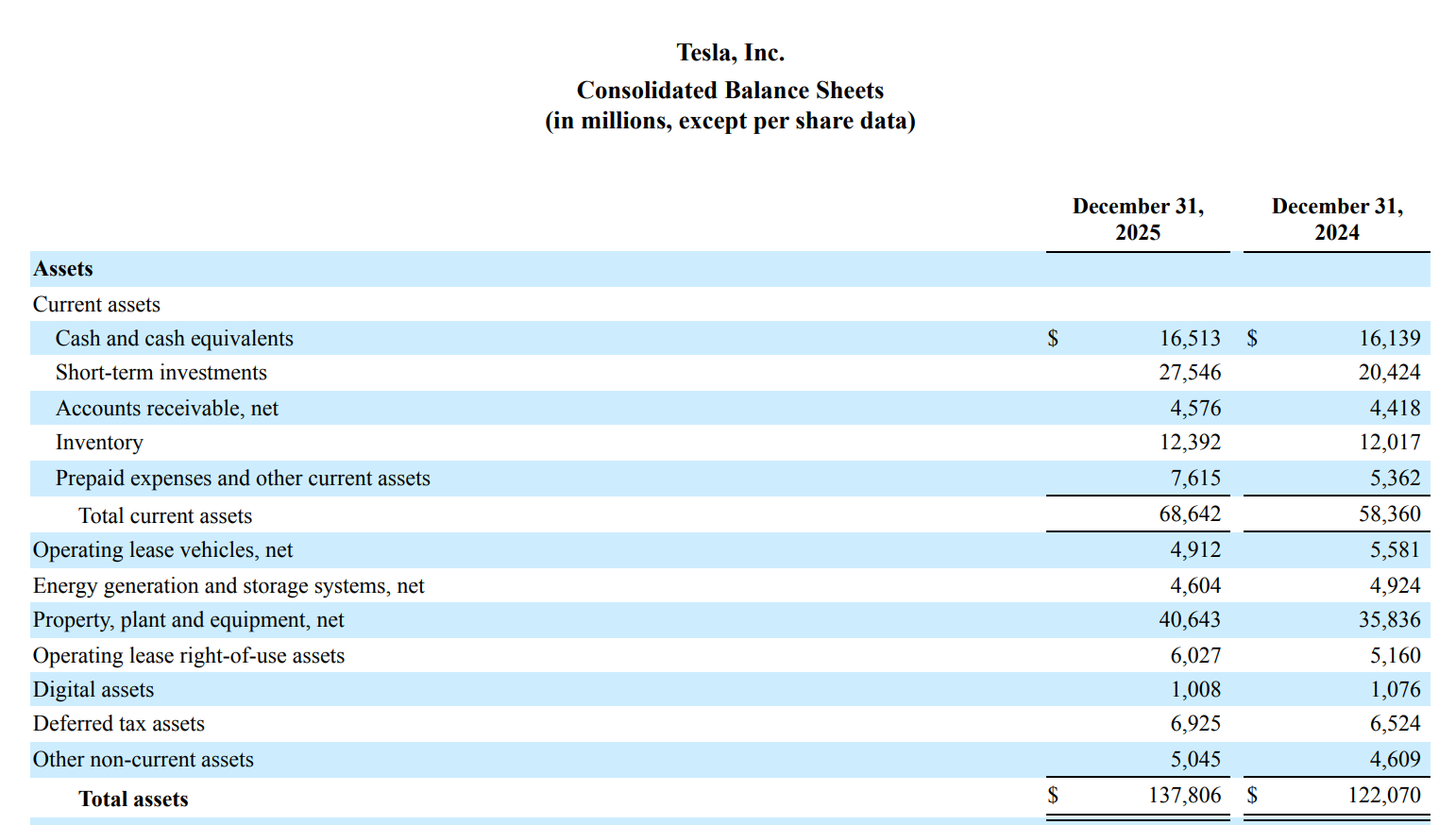

forty-four billion in cash. around fifteen billion in annual operating cash flow. and they just guided to over twenty billion in capex this year. six new factories, ai compute, infrastructure expansion.

this isn’t a company hoping narrative will fund its runway. they’re writing the check themselves.

and they’re burning the ships. discontinuing s and x to make room for optimus. converting factories. going all in on the identity shift.

i respect conviction. i’ve learned the hard way that half-measures don’t work.

but the story still has to become real. and that’s where i’m watching closely.

what the market is expecting.

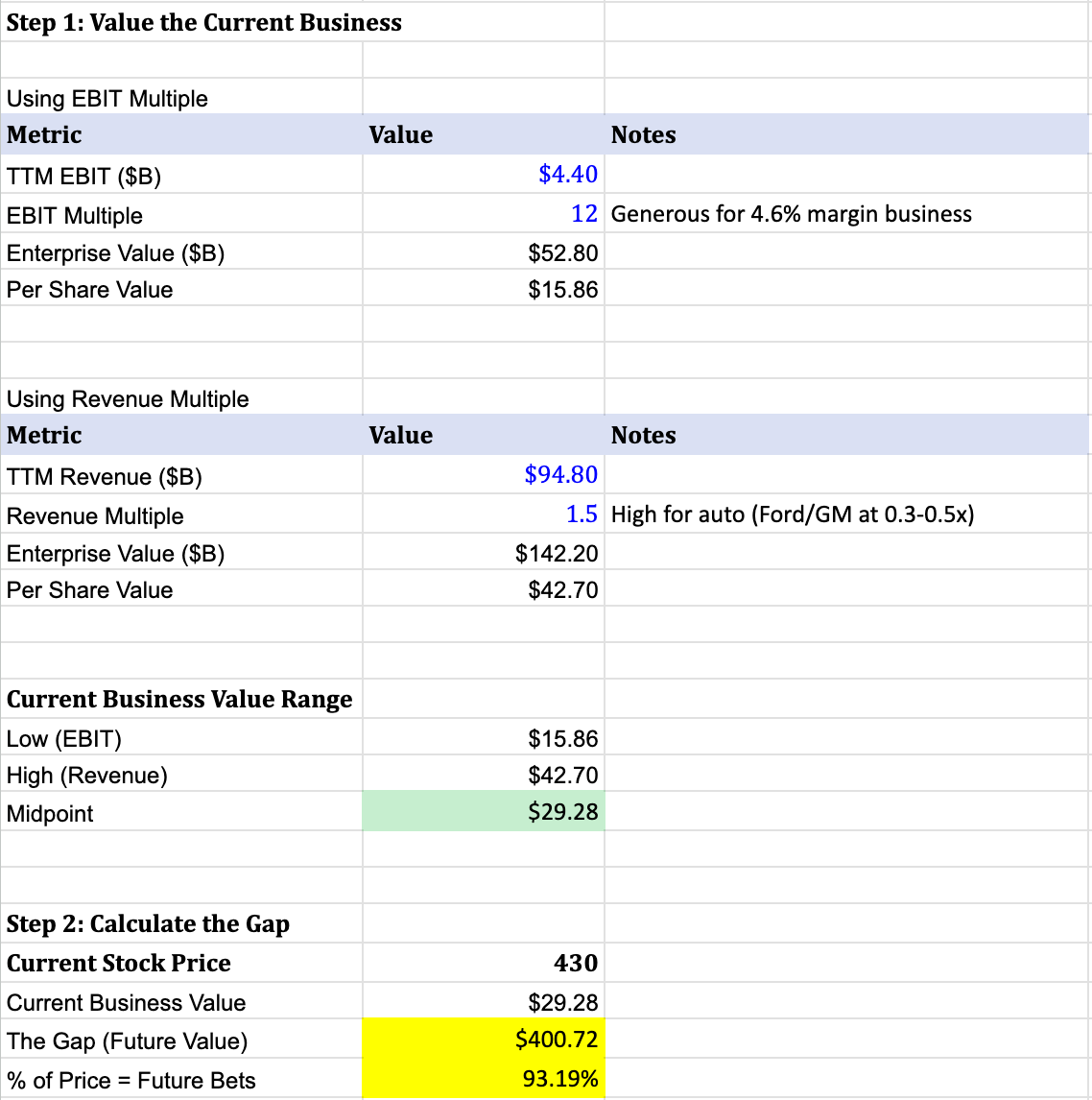

at four hundred thirty dollars a share, what are you actually paying for?

the reverse dcf breaks it down:

current business value. sixteen to forty-three dollars per share (seven to ten percent of the stock price).

ai/robotics optionality. about four hundred per share (ninety-three percent of the price).

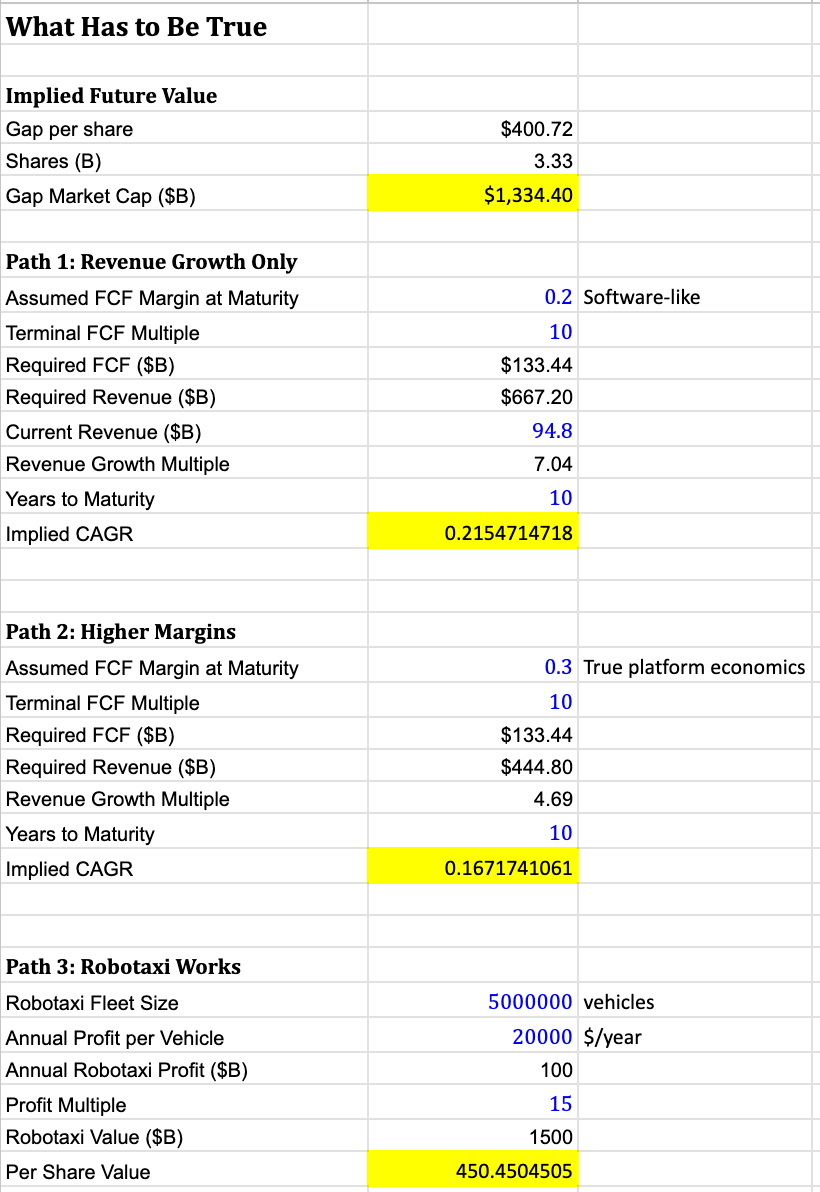

the market believes tesla will grow revenue six to seven times from here. ninety-five billion to five fifty or six sixty-five billion. that’s twenty-plus percent annual growth for ten years to fifteen years.

but auto is shrinking. energy is growing fast, but it’s only thirteen percent of revenue. so ai and robotics have to not just grow. they have to more than offset the decline in the core.

implied margins at maturity. fifteen percent or higher. current is four point six.

this isn’t a “show me” valuation. this is a “believe me” valuation.

let me show you something.

the reverse dcf splits the price into two pieces.

piece one. the current business. using an ebit multiple, about sixteen dollars a share. using a revenue multiple, maybe forty-three. midpoint around thirty. either way not much.

piece two. everything else. four hundred dollars betting on robotaxi, optimus, and ai infrastructure that hasn’t arrived yet. ninety-three percent of the stock price is optionality.

but here’s the caveat. i’m modeling something i can’t fully see. they’re spending twenty billion on capex next year. when do we get disclosure on cost per ride, margin per ride, utilization rates? until then, part of this is faith.

if robotaxi delays. if the story breaks. the stock reverts to car company multiples. fifty to a hundred dollars. seventy percent drawdown.

the math says you’re paying full price for a future that hasn’t arrived yet.

this isn’t a mispriced stock. it’s a binary bet.

either they become the physical ai platform and this goes to eight hundred, or the narrative breaks and it reverts to one thirty.

what i noticed.

automotive revenue dropped, but it tracked with deliveries. no pricing collapse. just softer demand. that’s different from a brand problem.

gross profit held despite the revenue decline. they’re doing something on the cost side. discipline showing up when it matters.

r&d spiked sixty percent. that’s not maintenance spend. that’s them putting money where the narrative is. ai, robotaxi, optimus.

they sunset the upfront fsd purchase. subscription only now. they want recurring revenue, not one-time payments. but it might also mean the eight thousand dollar option wasn’t converting.

elon said austin robotaxis are running “without chase cars.” reporting from days before said chase cars were still present. that gap. between what’s said and what’s verified is exactly what i’m watching.

energy had a record quarter. one point one billion in gross profit. this segment is becoming material while auto shrinks. and it’s not dependent on the robotaxi narrative.

how i’m seeing it.

i believe in the direction.

production is the moat, not software. i keep coming back to tesla as an infrastructure company. service centers, charging, manufacturing. the question isn’t whether fsd beats waymo on a benchmark. it’s who can actually scale hardware.

commodity dynamics protect against brand risk. if it’s cheaper, people take it. brand matters at the margin, not the decision. that’s a bet that price wins. and tesla is getting better at cost.

the owner fleet model makes sense to me. airbnb for cars. you let your tesla work while you sleep. the unit economics are intuitive if utilization is high enough.

but i’m skeptical on the price.

the story is ahead of the physical reality. digital ai is in millions of hands today. tesla’s physical ai is still in “trust us, it’s coming” territory.

same pattern i’ve seen before. someone says they’ve changed. the words are right. but i need to see it sustained before i believe it.

where i diverge from the bulls. the gap between narrative and physical reality is wider than it looks. surface signals aren’t enough for me.

where i diverge from the bears. the tam might be much bigger than anyone models. and in the ai age, narrative can sustain valuations longer than fundamentals suggest. plus they have the cash to keep building regardless.

the edge is patience. wait for the gap to close. either price comes down or reality catches up.

what would confirm this.

unsupervised robotaxis without conflicting reports

published safety data comparable to waymo

robotaxi revenue in the financials

unit economics disclosed

cybercab actually shipping in april

optimus actually in factories

proof, not promises. same standard i hold for anyone trying to show me they’ve changed.

if the price pulls back to one-fifty or two hundred, the risk-reward changes materially.

where i could be wrong.

time might be the weapon i’m underestimating. belief attracts capital, capital buys time, time delivers results. if they execute, four eighteen looks cheap in hindsight. waiting for proof might mean buying at six hundred.

and the reflexivity loop is real. tesla’s high stock price isn’t just a scorecard. it’s a currency. it lets them hire the best engineers with stock comp. the “bubble” valuation might be the fuel that builds the thing that justifies the valuation.

i could be wrong about the moat. i keep saying production, not software. but what if software is actually the bottleneck? what if waymo’s approach ends up winning because regulators demand it?

china is the risk i can’t model away. elon admitted it on the call. byd is eating the low end. xiaomi is moving fast. that’s where the brand premium erodes first. and geopolitically, that revenue concentration is a vulnerability.

some lingering thoughts.

what if waiting for proof is the wrong frame? what if belief is the catalyst that makes the proof possible?

why is elon spending saturdays on chip design? what does that tell you about where he thinks the bottleneck is?

how long can the balance sheet buy them before the market demands results?

where could i get hurt even if my thesis is right? timing, position size, opportunity cost?

what if patience is just a story i tell myself to avoid risk?

the history lesson: a documentary on hitler. sounds unrelated. but i've been thinking about the last time geopolitical tensions were this high. how narratives build. how belief compounds. how people saw the signs and stayed anyway.

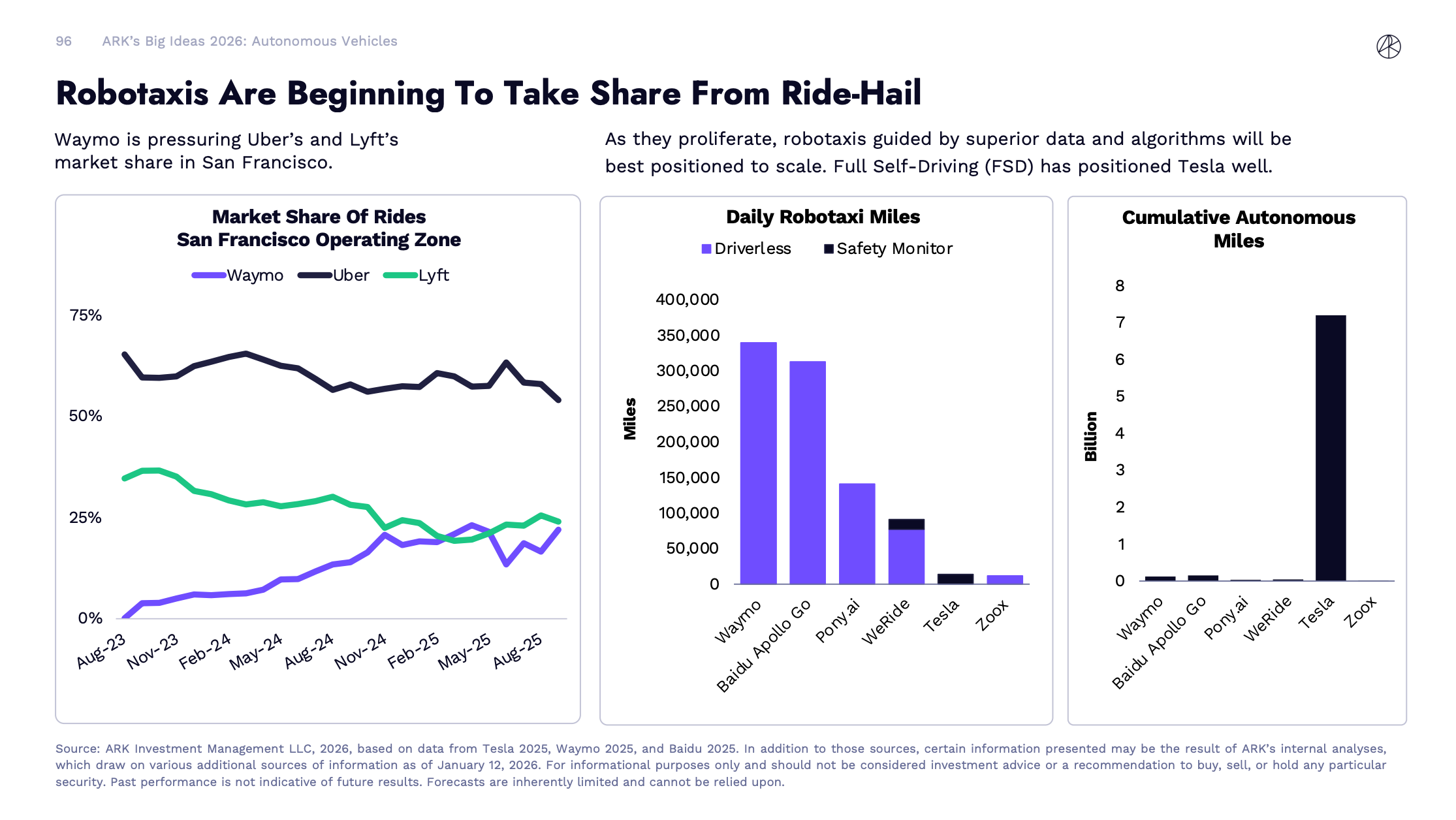

the chart: tesla has the miles. waymo has the rides. the gap.

the read: bill gurley on tam. the ride he thought would take thirty minutes took five. the market wasn’t what he modeled. it was ten times bigger.

the question i can’t shake: what does it cost to need proof before you believe?

still thinking about that launch. the sound of it. watching something actually take off.

i don’t know if this is that. but i’m not looking away.

— b.