the plumbers come first

a syllabus on the physical layer beneath the ai story. five things. 4 min.

no agenda.

oat latte’s hot.

sit down. laptop open.

last month i hit “you’ve reached your usage limit” on claude in the middle of a workday. not surprising. it’d been happening more. but this time i sat with the popup instead of refreshing. somebody, somewhere, decided i needed to stop. and the reason wasn’t software.

a few weeks earlier i’d been listening to jensen huang on dwarkesh. he said the thing that flipped it for me. the bottleneck on the next decade of ai isn’t an algorithm. it’s plumbers and electricians. shortage of trades. transformers on backorder. substations waiting on permits. dario amodei said it from the demand side. anthropic planned for 2 or 3x growth. the business did 80x and has since blown past a $47 billion run rate. “the constraint becomes physical infrastructure.” altman said it shorter. openai’s chips were overheating from how many people were using chatgpt.

the rate-limit popup and the plumber are the same story.

by plumber i mean the whole physical layer beneath the model. the electrician. the hvac tech. the substation. the chip. the cooling tower. the water pipe. everything the model is quietly sitting on top of.

the lesson.

claude. chatgpt. gemini. the new ai app that shipped this week. each of them is in a different fight with the chips, data centers, power, and water they need. some can still absorb demand. some are already constrained.

the wall you hit on a tuesday afternoon is infrastructure talking back.

the syllabus.

five things to sit with. in this order if you can.

each one's a link. open it, sit with it, come back.

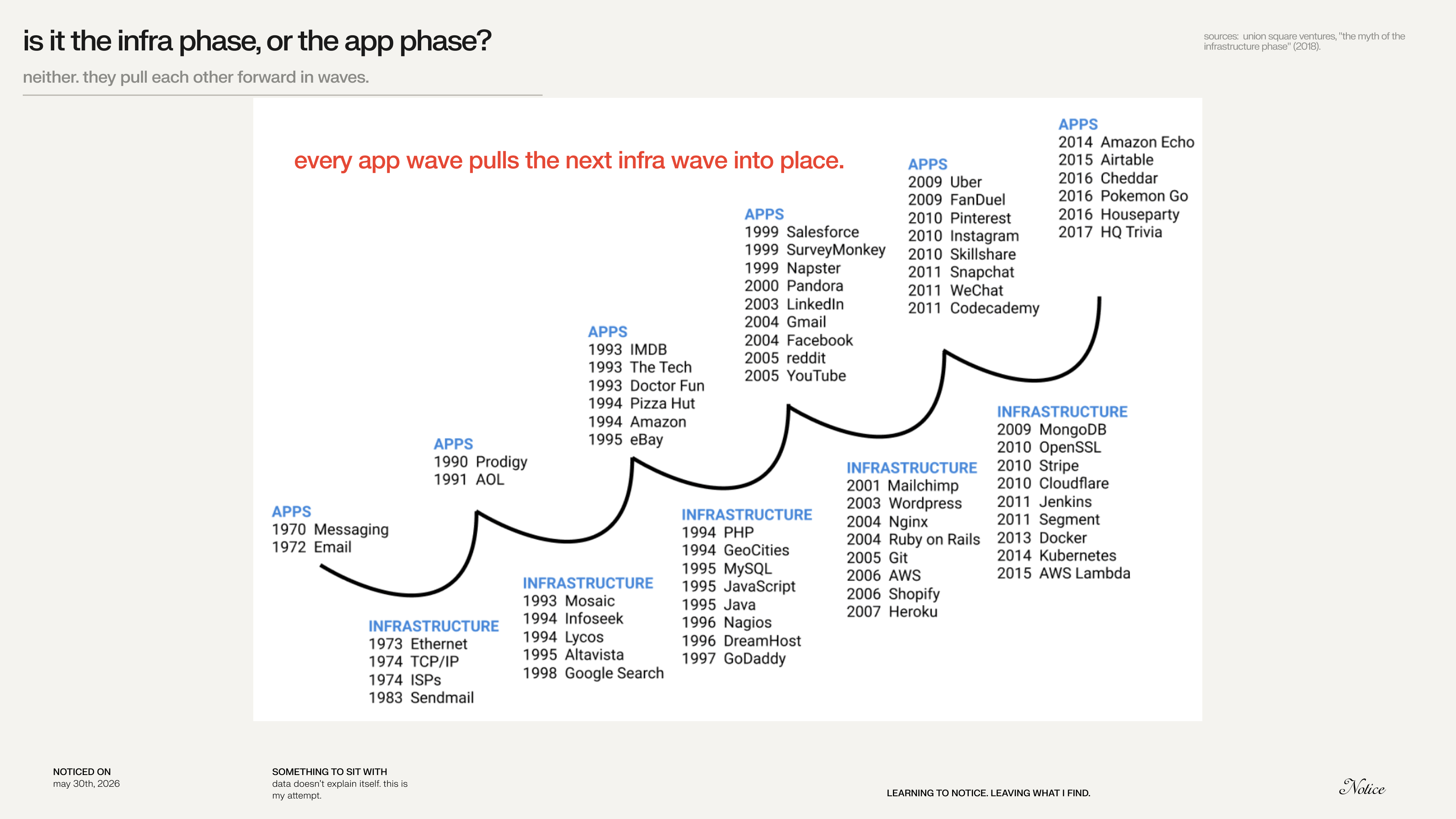

i. usv, the myth of the infrastructure phase. ↗ read

the spine of this whole piece.

dani grant and nick grossman push back on the idea that we move through clean “infrastructure phases” followed by “app phases.” they argue infra and apps pull each other forward in loops. apps create demand. demand pulls new infra. new infra unlocks new apps.

things to notice:

once you see the loop, you stop asking “are we in the infra phase or the app phase.” you start asking which side is pulling harder right now.

the rate-limit popup is the application side pulling new infrastructure into place in real time.

sit with these. then take them to claude.

which ai product can do something this year it literally couldn’t last year, and what got built underneath to make that possible?

which piece of infrastructure is getting ordered right now because an app blew past everyone’s expectations?

what other industry runs on this same loop and nobody calls it that?

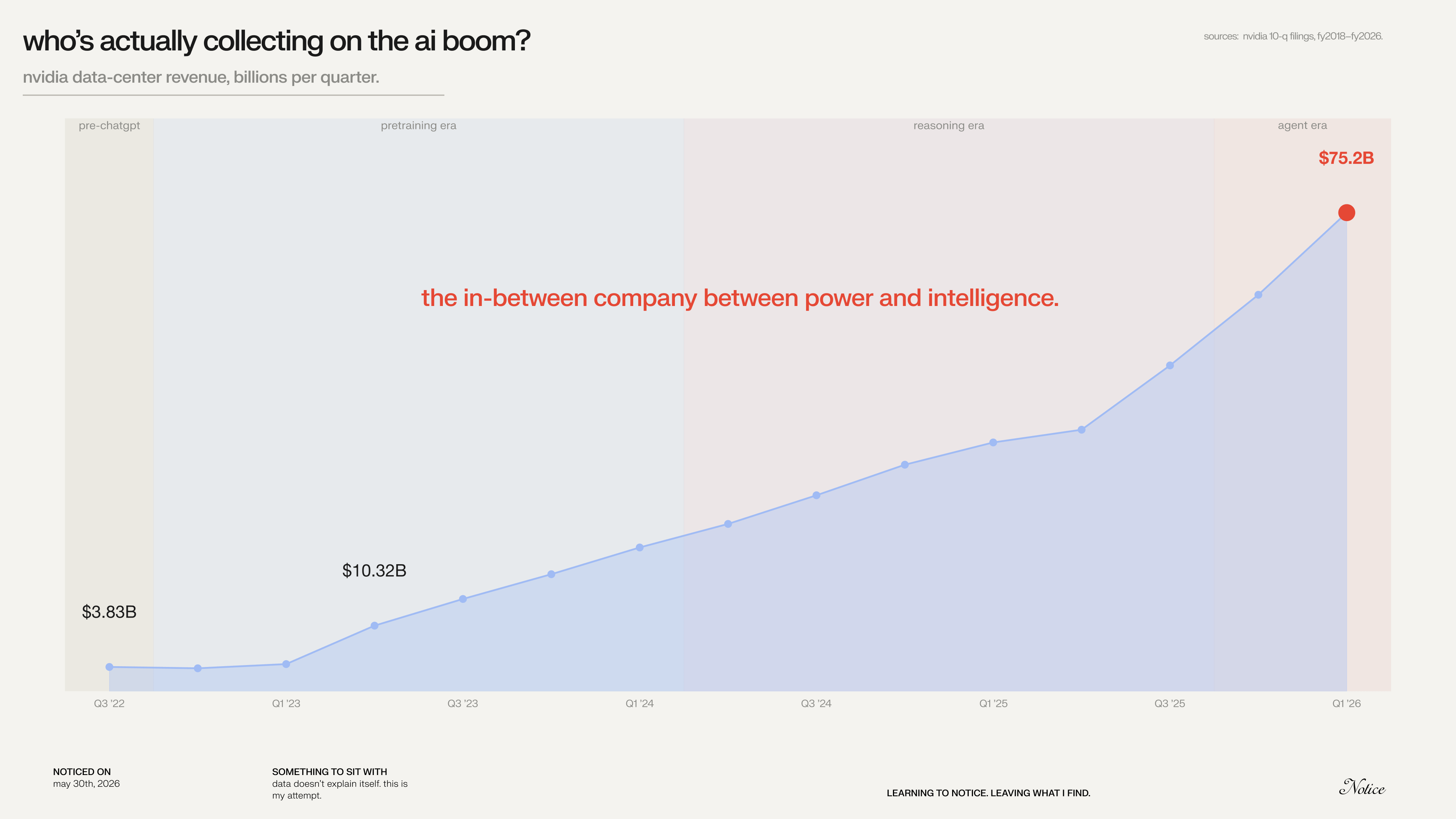

ii. jensen huang on dwarkesh. ↗ listen

the framing.

jensen describes nvidia as “the in-between.” electricity goes in. tokens come out. one sentence reorganizes the whole map of the ai business. it’s an industrial company, not just a software one.

things to notice:

listen for the part about elon having more nvidia chips than openai and anthropic combined.

pay attention to how often he talks about energy, throughput, and factories instead of “ai magic.”

sit with these. then take them to claude.

nvidia turns electricity into tokens. what’s the next “in-between” company nobody’s named yet?

if elon is sitting on the most compute, what does he have to ship to turn it into revenue?

where’s the chokepoint inside the inference economy itself?

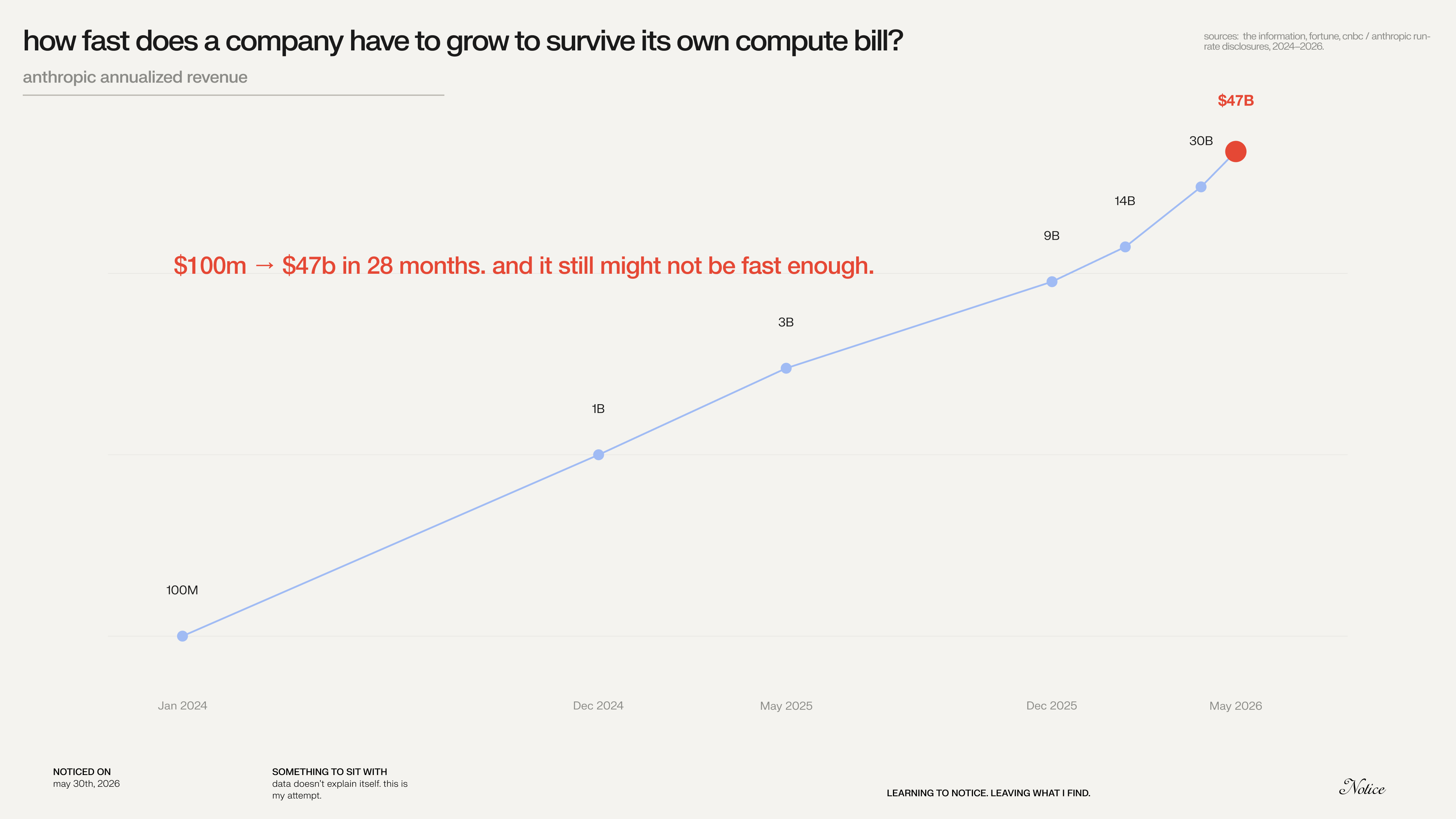

iii. dario amodei on dwarkesh. ↗ listen

the math.

dario said: “if my revenue is not $1 trillion, if it’s even $800 billion, there’s no force on earth that could stop me from going bankrupt if i buy that much compute.” every weekly cap on claude is downstream of that one sentence.

things to notice:

listen for what he thinks anthropic’s revenue actually has to look like by 2028 to make the spend safe.

the existential risk for anthropic isn’t a bad model. it’s the bill.

sit with these. then take them to claude.

if dario is right, what does using claude or chatgpt feel like in 2030?

who’s writing the check that keeps anthropic alive in 2028?

does the winner end up being the smartest model, or the one that figured out how to pay for itself?

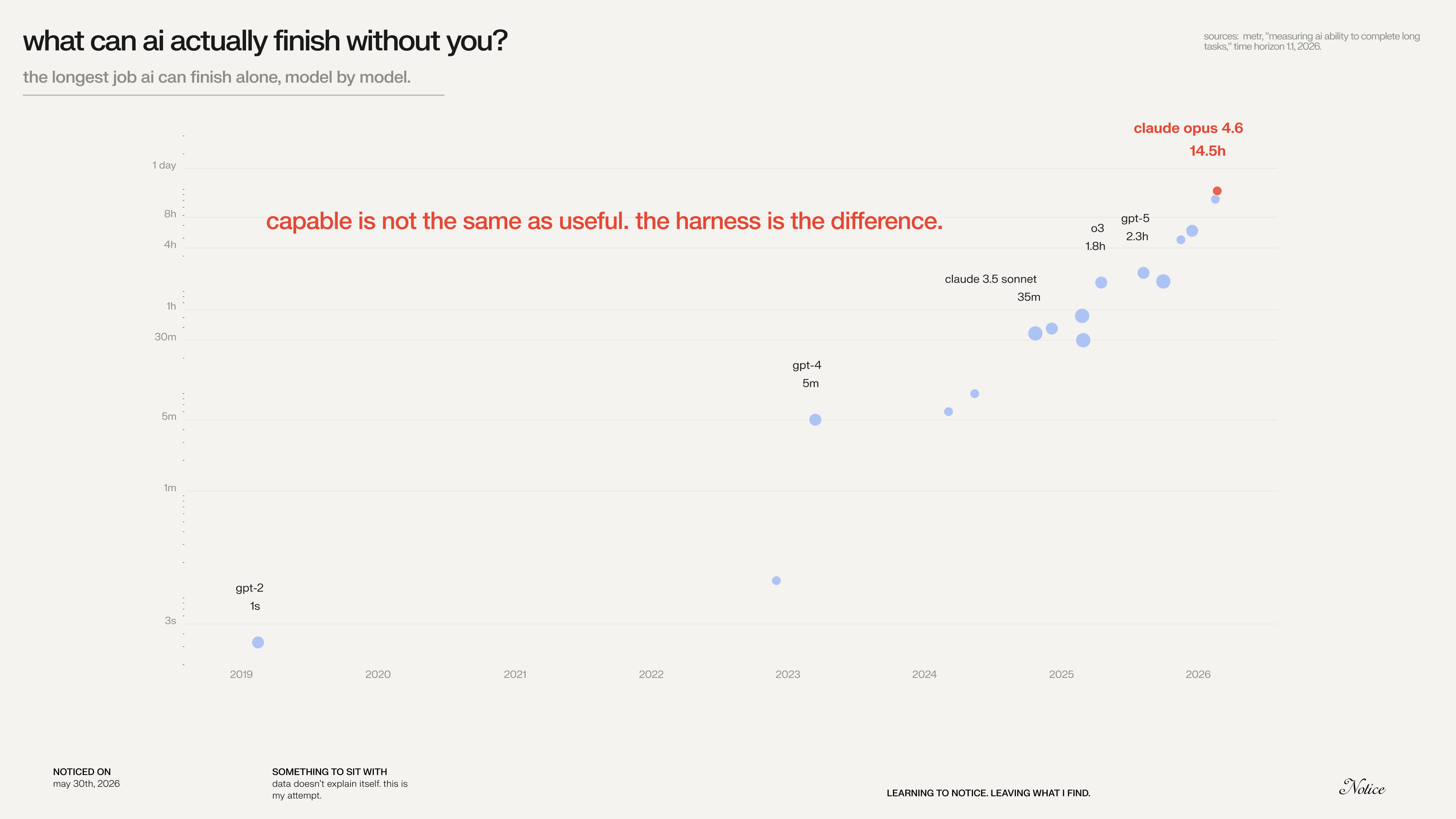

iv. ben thompson, agents over bubbles. ↗ read

the economics.

thompson argues an “agent” is a model plus a harness. the moat lives in the harness. the infrastructure, the integrations, the runtime. not the weights. if he’s right, the whole “best model wins” frame is wrong.

things to notice:

the valuable layer may not be the model. it’s the system wrapped around the model.

every successful harness drives more compute demand underneath it. harness winners and chip winners aren’t opposed. they pull each other.

sit with these. then take them to claude.

which boring office task that took you hours or days just became automatable because of opus 4.7 agent capabilities?

which workflow nobody’s wrapped yet could be worth more than the model running underneath?

which job is one capability away from being done by software, not a person?

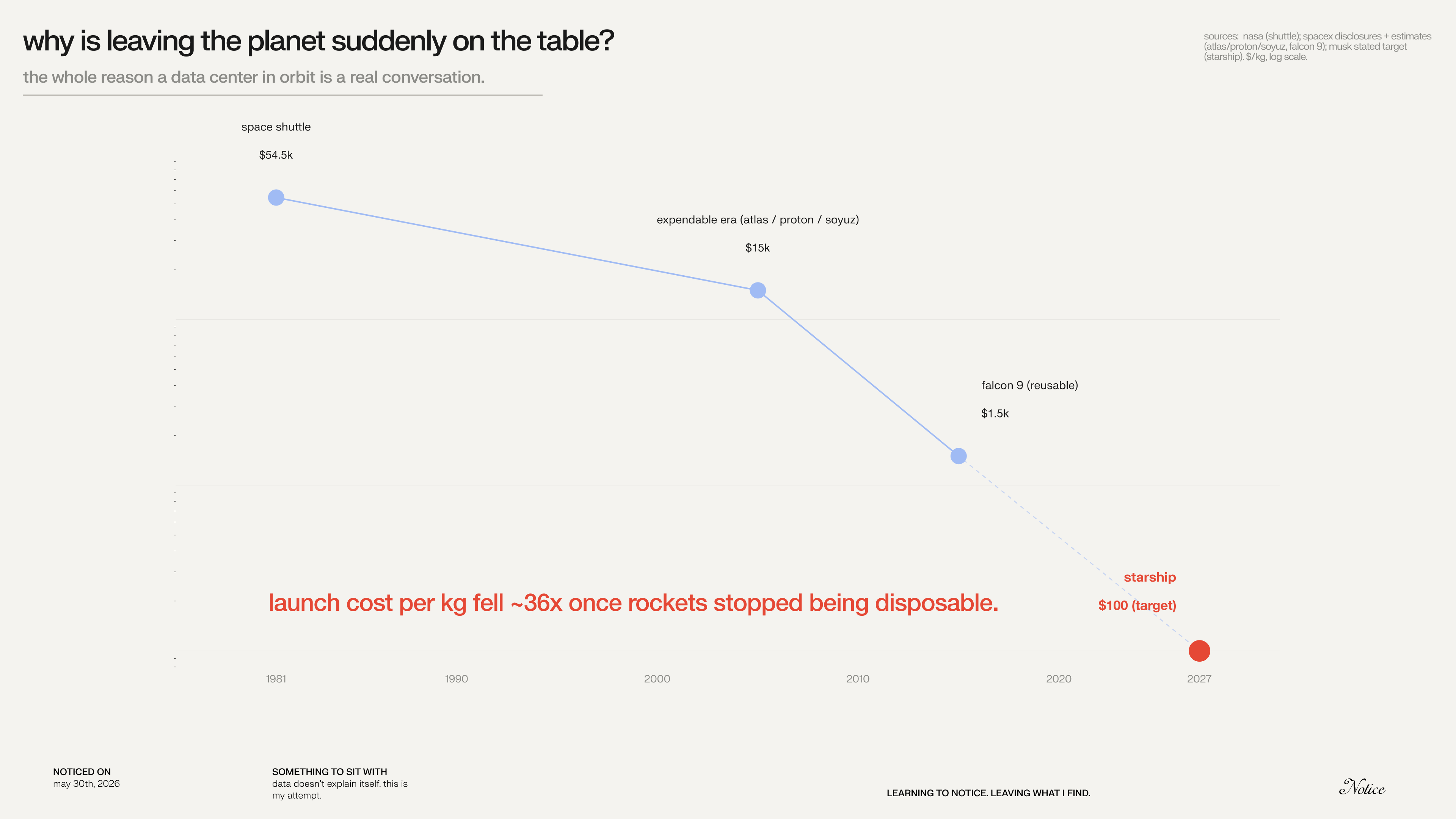

v. gavin baker on orbital data centers. ↗ listen

the frontier.

baker on what happens when “more power, more land, more cooling” stops being something you can permit on earth. cities are already banning data centers. the response is to leave the planet.

things to notice:

the picture in your head is probably wrong. it’s not pentagon-sized facilities in orbit. it’s racks.

the deeper idea is that compute is becoming geographically mobile. it doesn’t have to live in a building.

sit with these. then take them to claude.

if a rack can run in orbit, what’s the next strange place compute ends up? underwater. in your car. on a balloon. what does each one unlock?

what else are we about to launch into orbit because we ran out of room down here?

what becomes possible when compute is no longer tied to a building?

so. look upstream. what else has to grow to support the ai you’re using?

— brylan.