for who they are

a page on figma. sit with it. 11 min.

what’s playing: lock in. — gunna, key glock, babyface ray.

i’ve been wrestling with figma for weeks. filings. transcripts. building a model just to argue with my own model. the fun has been the wrestling itself.

what i keep coming back to is the gap. between what the market is saying about figma and what figma is actually doing. between the picture and the felt-thing.

i’ve felt this one before. dinner went fine. the movie went fine. the picture from the outside was clean. the felt-thing underneath was something else. you can talk it out. it doesn’t change the past.

that’s the shape of this page. that’s also the shape of figma right now. the market is debating whether ai kills figma. the real question is whether figma is still where software gets made.

how this kind of business works.

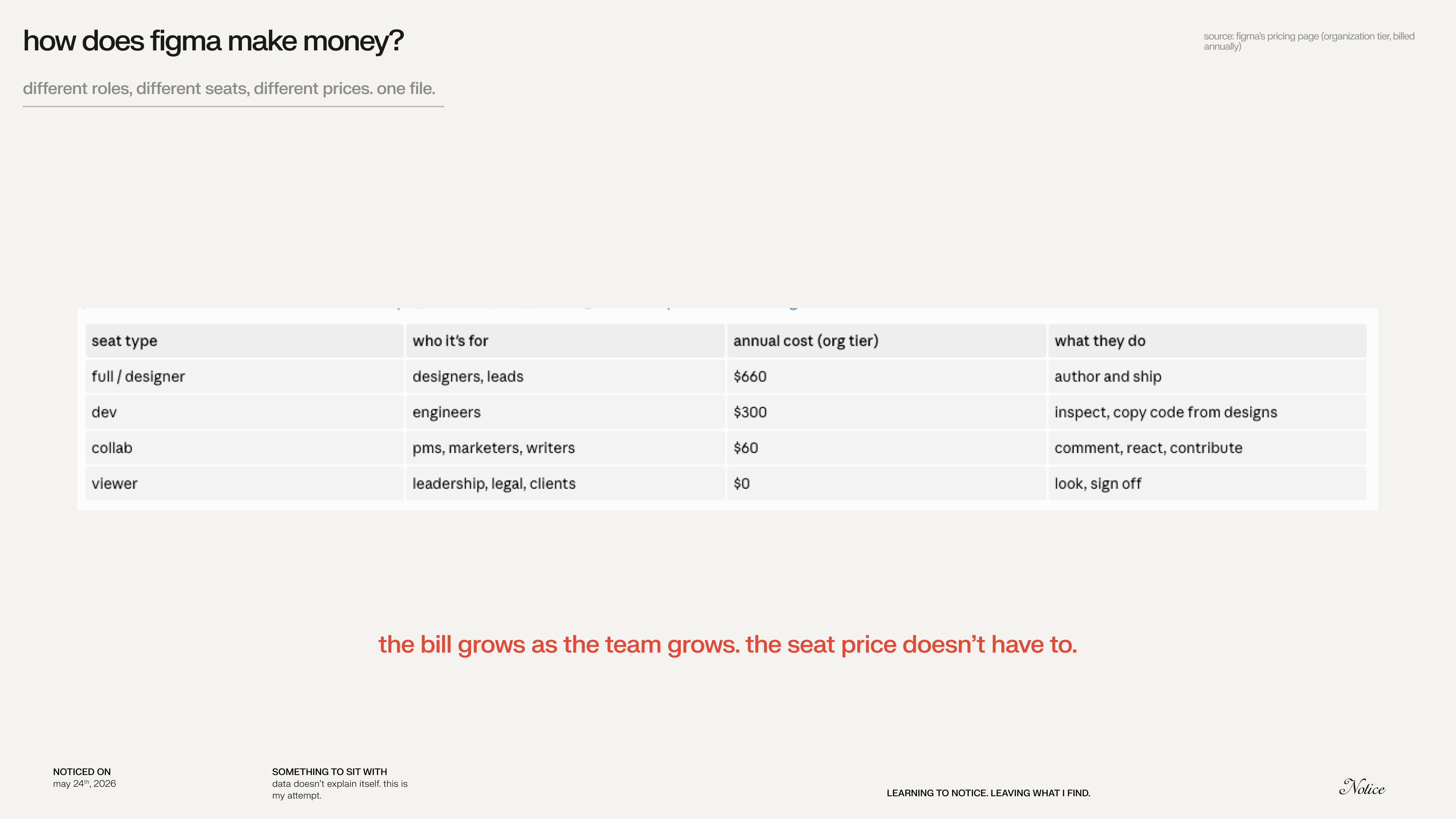

figma sells a file. the rest is dressing.

the file is a multiplayer browser canvas where designers, developers, pms, and now ai agents meet to build software. before figma, designers worked in sketch, exported pngs, and emailed them around. figma did to design what google docs did to word. it made the file the meeting place. once the meeting place is yours, every adjacent workflow becomes a feature you bolt on and charge for.

they charge by seat, sliced by role. designer. developer. collaborator. content. same playbook as office charging readers, writers, and editors different prices for the same documents. when a big customer adds engineers and marketers over time, the bill grows even if the seat-price doesn’t.

here’s the wild part. the customers who paid figma more than ten grand last year are paying thirty-nine percent more today. same customers. one year later. thirty-nine percent more. that’s after everyone who quit, every downgrade, every account that got rationalized. the bill grows because the file grows into more of the building. the engine works. that’s the part to remember.

the story being told.

i watched it drop. read the substack posts. felt the panic on twitter.

the story is that ai is killing figma.

it’s loud. plaintiff law firms circling. anthropic’s head of design left to ship a figma competitor. she was figma’s own director, the one who built figjam and slides. google launched two design products in march. anthropic launched claude design in april. every drop has had a date and a story attached. that’s what makes it so easy to tell.

the case has a name. ai bundling. anthropic and google and lovable give designers most of what figma gives them, for free, inside the same window they already use for code. small users leave first. enterprise follows. the spending-more pattern breaks. figma becomes adobe at half the price.

that’s the market. that’s what’s loud right now.

what the market is expecting.

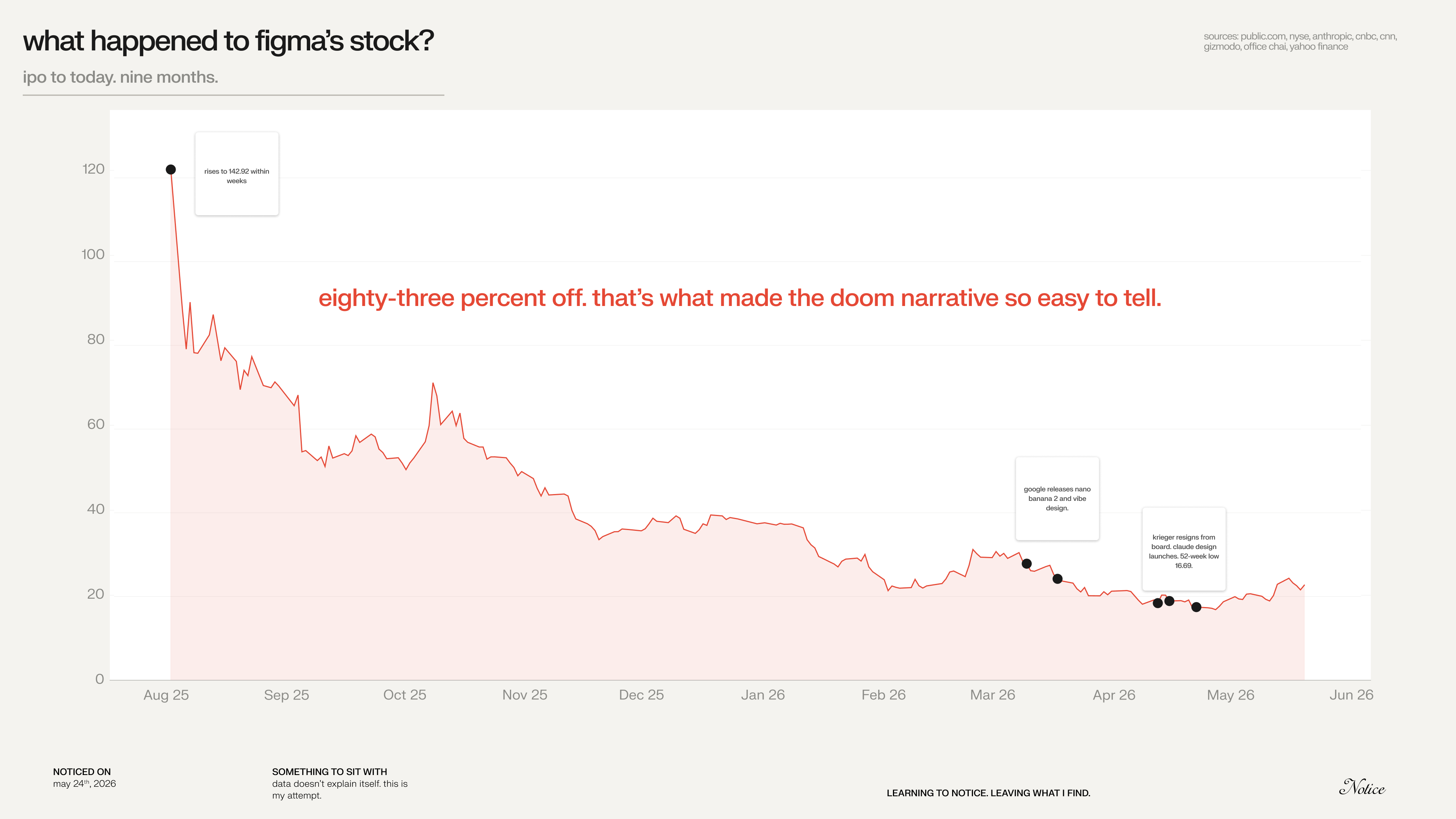

figma went public august 1st, 2025. it ripped to a hundred and forty-two ninety-two within weeks. nine months later it touched sixteen sixty-nine. today it sits at twenty-two fifty-two. eighty-three percent off the high.

to price a stock down that hard, the market needs a story.

i built the model to figure out which story. sat with it for a week. it kept asking me what i actually believed about the next three years.

here’s the one it’s telling.

designers don’t have to draw anymore. type “build me a settings page that matches our app” into claude or cursor or v0, and the ai ships working software in seconds. no mockup. no figma file. no handoff. jenny wen said it on lenny’s podcast in march. the design process is basically dead. she’s anthropic’s head of design now. former figma director. figma was the venue for the old way.

if she’s right, designers shrink as a role. fewer seats sold. customers who used to spend more start spending less. ai is expensive to run, so the dollars figma keeps cost more to deliver. investors decide each dollar is worth less. figma ends up looking like adobe at half the price.

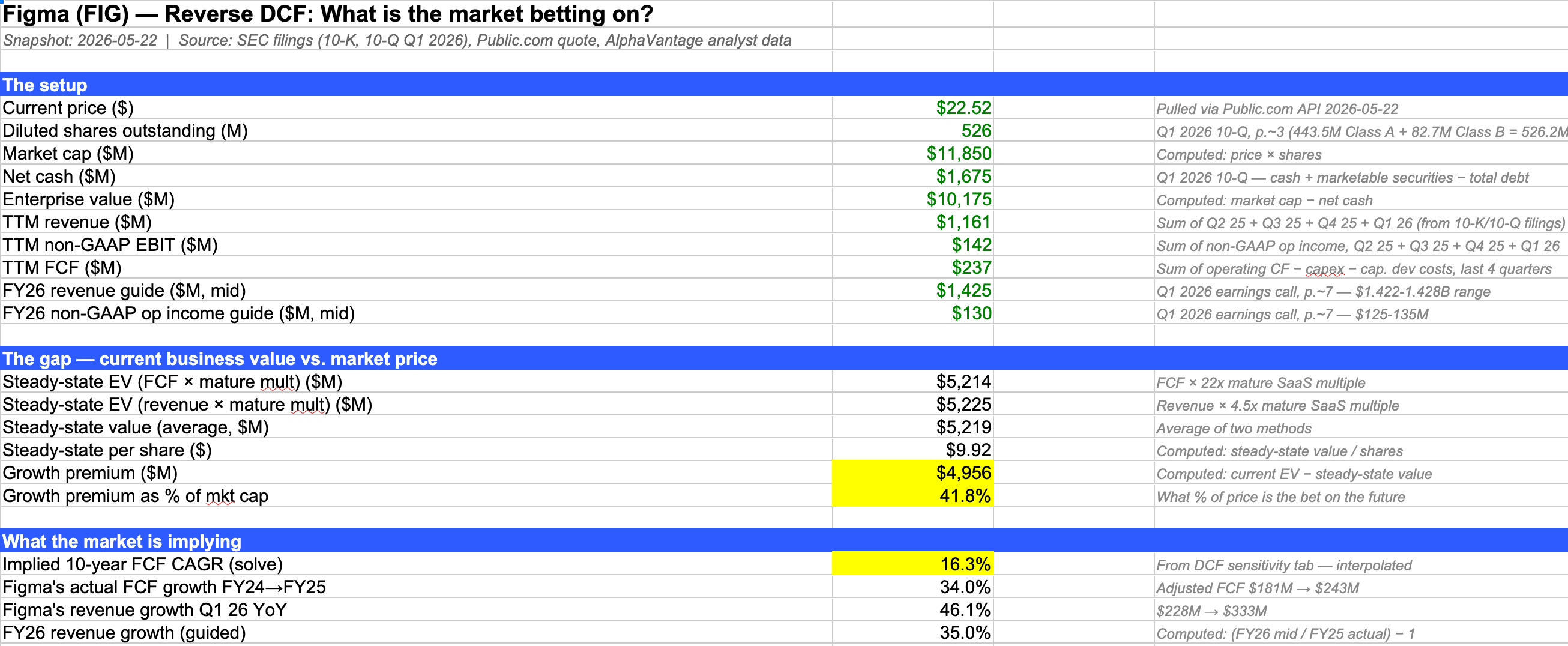

that’s the bet. at twenty-two dollars and fifty-two cents, the market is pricing it. figma’s cash grows sixteen percent a year for the next decade. not the thirty-five they’re currently telling wall street. claude design and canva take real customers. all of it has to be roughly right for the price to be roughly right.

i built the model. screenshot below. file linked at the bottom.

two more things. eleven percent short interest. about six million shares betting figma falls further. anything good prints, they have to cover into a thin tape.

and a stock moves on two engines: the dollars the company makes, and what investors will pay per dollar. they can move opposite ways. goldman cut their price target to thirty dollars in april and raised the dollars they expect figma to make. the damage was investors paying less per dollar. not figma making fewer.

let me show you something.

i read the print twice. once for what it said. once for what it didn't.

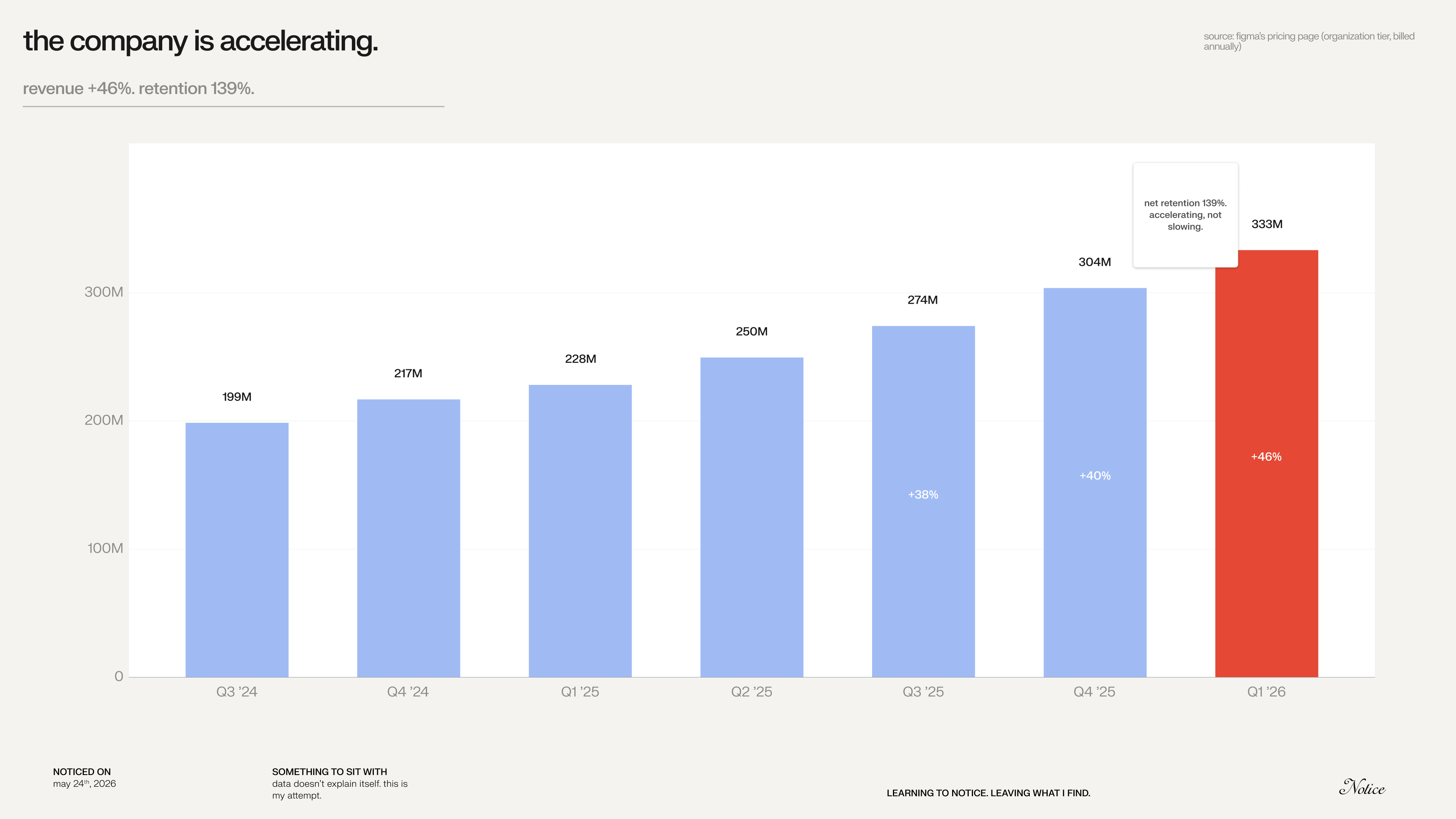

ten days ago, figma reported its first quarter. revenue up forty-six percent from a year ago. the customers-spending-more thing? they went from spending thirty-six percent more to thirty-nine percent more. accelerating, not slowing. after paying to deliver the product, figma still keeps seventy-nine and a half cents of every dollar. after paying the bills, they keep sixteen cents. they’d told wall street to expect nine.

three out of four of the bigger customers used figma’s ai features in the most recent week. that’s people leaning in. the opposite of leaving.

the price implies sixteen percent long-term growth. the company printed forty-six. that’s the gap. that’s the whole trade.

what i think.

who is figma, actually? not who figma is to the substack writer who tried claude design over a weekend. who figma is to the seven out of ten customers buying more than one of their products. who figma is to the customers spending thirty-nine percent more this year than last. a company where designers are now a minority of the people inside the building. where engineers are the fastest growing group. where every new ai feature is another way to charge, not another way to lose.

the right comparison isn’t adobe. it’s coordination. github. slack. atlassian. companies that got more valuable as the work they coordinated got harder, not less. if engineers become the largest seat type inside figma, figma stops being “design software.” it starts being where teams of humans and agents meet to make software.

that’s a different company than the one being shorted.

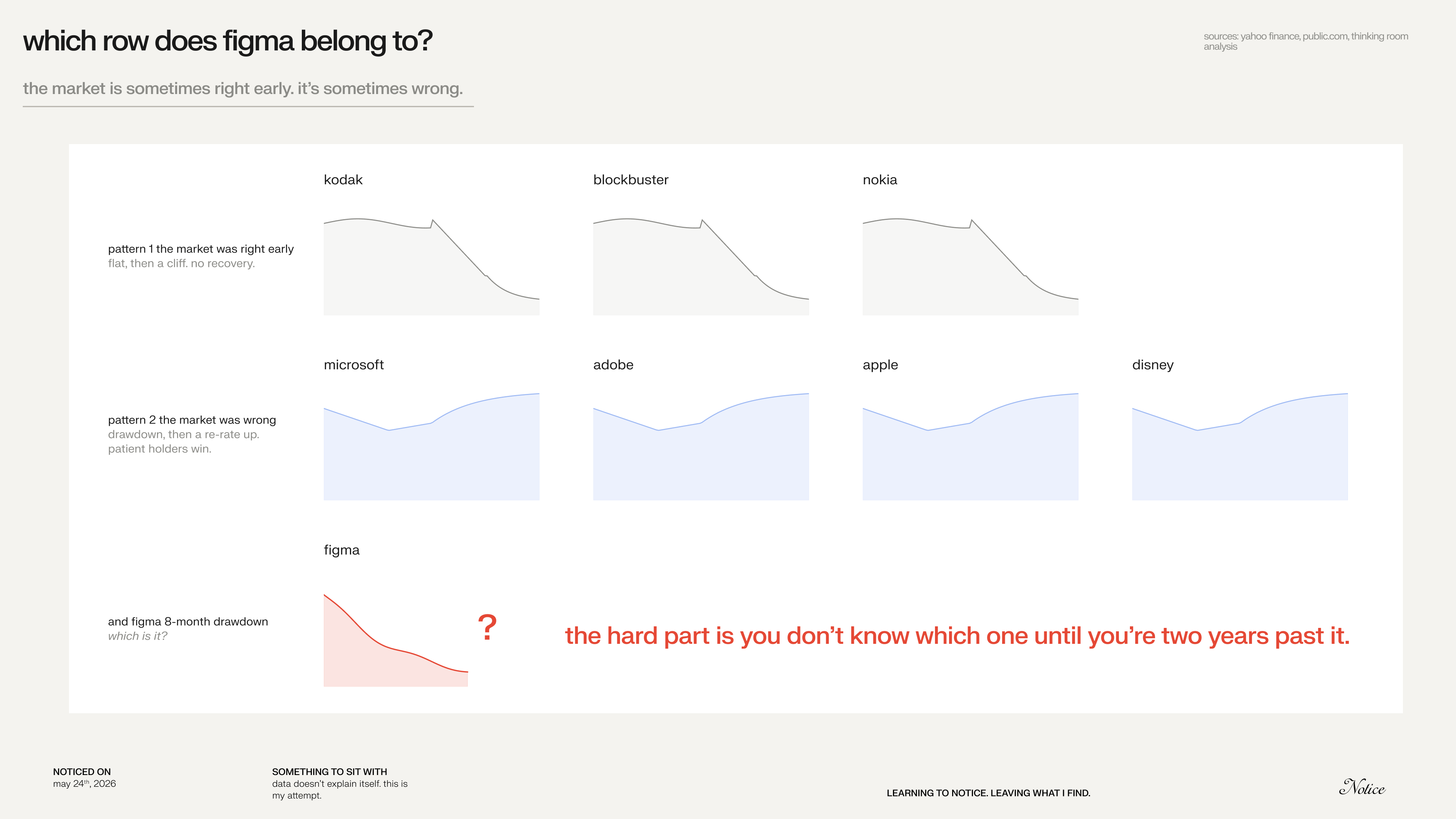

history has two shapes for moments like this. in one, the market is right early. kodak. blockbuster. nokia. numbers look fine for a while. then they don’t. in the other, the market is wrong. microsoft in 2014. adobe in 2011. disney through streaming. the story said extinction. the numbers said adapting. the stock eventually followed the numbers.

the evidence so far points toward pattern two. a figma director put thirty-six and a half million dollars of his own money into the stock in february. cathie wood added eight million in march, after google launched. the bigger customers are spending more, not less.

dylan field is the other tell. defensive language is what you’d expect from management watching the funnel break. instead, figma raised expectations through the panic. quietly started training their own ai model in august 2024, twenty-two months before config. spent around two hundred million buying weavy in october. people running for the exits don’t do that.

here’s the deeper reason incumbents sometimes survive these moments. ai changes how a single artifact gets generated. it does not change the work of getting a hundred people aligned on which artifact to ship. governance. approvals. design systems as infrastructure. multiplayer state. enterprise memory. auditability. the file isn’t valuable because it’s hard to make a mockup. it’s valuable because it’s where the company decides what to build. coordination is the moat that doesn’t go away just because generation got cheap.

history rhymes here. the cloud commoditized compute, and orchestration layers became valuable. open-source commoditized software, and the workflow layers became valuable. ai might commoditize interfaces. if it does, what becomes valuable is whatever does governance, alignment, and coordination across humans and the agents now in the market with them. figma is closer to that surface than anyone in the market is currently pricing.

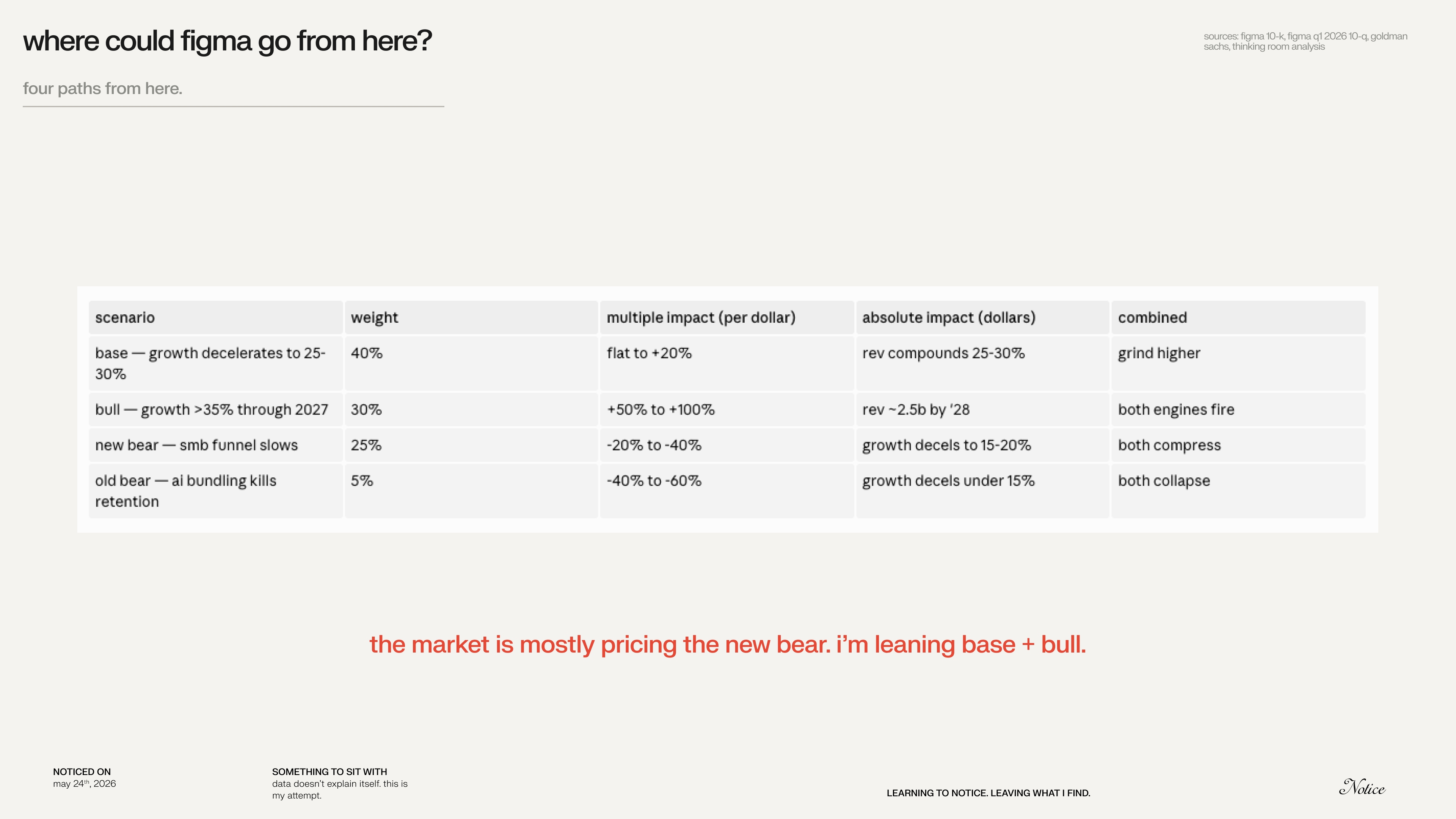

but at this stage in 1996, microsoft looked like pattern one too. you don’t know which one you’re in until you’re two or three years past it. my confidence the case for figma is defensible. that a smart person could argue it without lying. sixty out of a hundred. my confidence figma actually wins over the next two and a half years. forty.

the market is shorting a 2027 obituary that 2026 keeps refusing to print.

the edge.

i'll admit it. i bought the consensus story for a minute. it sounds smart. it's been wrong for a year.

the case the market is repeating goes like this. ai makes figma’s customers spend less. it has been wrong for four straight quarters. they’re spending more. the prediction is dead. the price still acts like it’s alive.

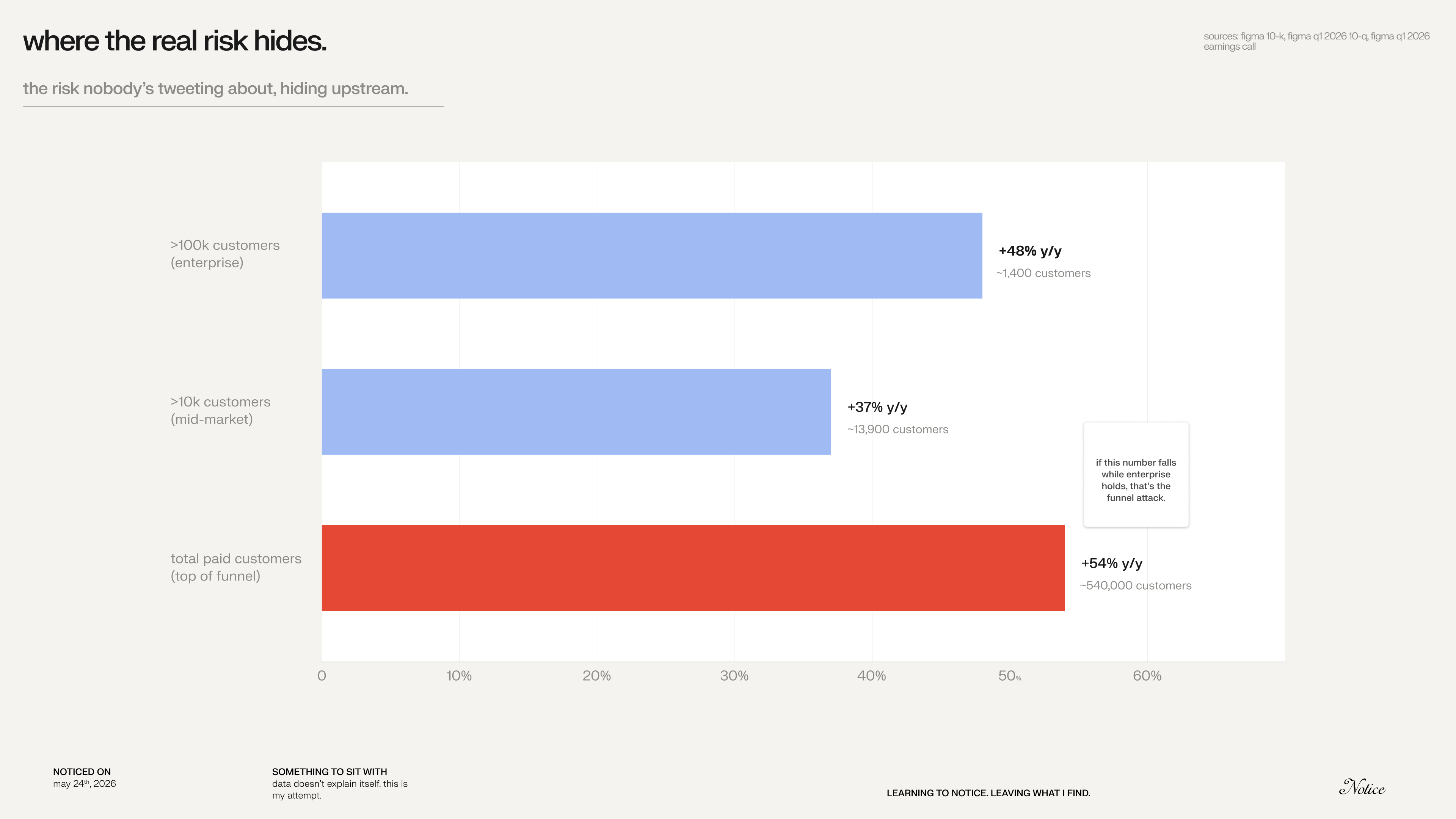

the real risk is harder to see and harder to tweet. it’s not that customers spend less. it’s that fewer new customers show up at the door. canva picks off small teams before they try figma. claude design picks off the people who’d have mocked something up over a weekend. figma becomes a company that sells only to big enterprises and grows slower. by the time you see it in the numbers everyone watches, it’s already been true for years.

the market is debating whether ai kills figma. that fight is settled in figma’s favor for the next four to six quarters. the real question is whether the top of the funnel is already silently broken. we won’t see it until contract renewals roll through in 2027 and 2028.

that’s where i diverge.

what would confirm this.

i have these two dates circled.

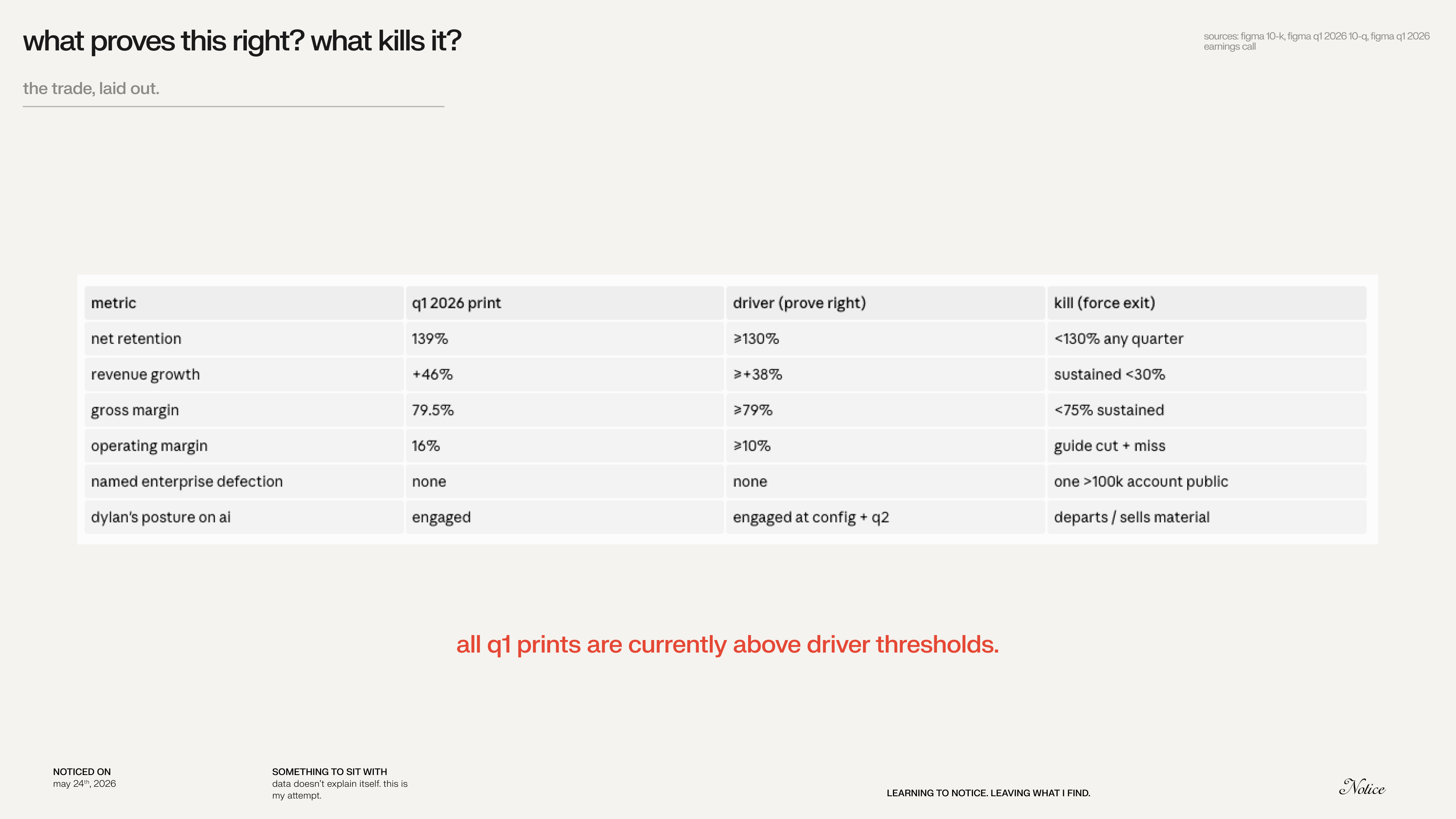

here’s what i’m actually watching. three drivers and four kill conditions. all of them resolve at the next print or before.

drivers that prove the hypothesis right:

the bigger customers keep spending more. the net retention number stays above one hundred and thirty percent. it’s a hundred and thirty-nine today.

revenue stays up at least thirty-eight percent from a year ago. it was forty-six this quarter.

figma keeps at least seventy-nine cents of every dollar after delivering the product. it was seventy-nine and a half this quarter.

after the bills, they keep at least ten cents. they kept sixteen this quarter.

the ai features start showing up as real money on the income statement. quantified, not hand-waved.

dylan ships figma’s own ai model at config. trained on the billions of files figma owns. with a real number showing it beats claude or openai on design tasks.

kill conditions. any one of these and i exit:

the net retention number prints below a hundred and thirty in any quarter.

a named enterprise customer publicly cuts its figma seats and cites a claude design or stitch.

two quarters in a row of fewer than five hundred new ten-thousand-dollar customers.

dylan field departs or sells a material insider stake.

two dates carry the test. config 2026, june 23rd through 25th, thirty days out. q2 2026 earnings, august 18th, eighty-six days out. config is the strategy read. q2 is the numbers read. together they tell me whether to ride the option or close the position.

this isn’t a forever bet. it’s an eighty-six-day bet with defined exits.

where i could be wrong.

the part i keep losing sleep over isn’t in the financials. it’s the workflow.

old way: idea → figma → review → engineering → code → deploy.

new way: idea → prompt → generated app → iterate live → deploy.

if the new way wins, the question of where collaboration happens stops having figma as its default answer.

jenny wen isn’t alone. lovable does a hundred thousand new projects a day. cursor runs in eighteen percent of professional developers at work. v0 has six million developers. these tools aren’t on most people’s radar yet. time-to-idea is collapsing in a place i cannot fully see.

the honest version. i can model the financials. i can’t model the shift in how product gets built with the same conviction. the real risk isn’t ai killing figma. it’s a new shape of work where figma isn’t the venue. big company contracts run one to three years. the spending-more pattern can hold for another four to six quarters before this shows up. then it shows up all at once.

the picture and the felt-thing can stay split for a long time before anyone knows which one was real.

some lingering thoughts.

if i’m right about the prints but wrong about the workflow, how long does the trade have before the architecture question catches up to it?

where does coordination actually live in an ai-native software stack? if it’s not the figma file, what is it?

what does jenny wen know from inside anthropic that the figma prints haven’t shown yet?

am i sympathetic to figma because i use it every day?

the market is loud about the wrong thing. the case it’s repeating has been wrong for a year. the case i’m actually worried about is invisible right now. the numbers say one company. the stock says another. the next ninety days will tell us which one we’ve been looking at.

the work, for any of us, on any company we’re trying to read, is seeing them for who they are. not who the market says they are. not who we wanted them to be. who they actually are when you sit with them long enough. figma’s real question isn’t whether ai kills it. it’s whether it’s still where software gets made. the answer to that one won’t come from august.

i haven’t seen what i need to see yet. but i’m sitting closer.

and i’ll tell you straight. i bought a long-dated call on figma earlier this month. thirteen hundred and twenty dollars. skin in the game. not a recommendation, not a heavy bet. the size that says i think this, but i could be wrong, and i want to be honest about both. writing a page like this without telling you would be hiding the ball.

the option runs to january 2028. the bet is ninety days. if config and q2 deliver and the stock pops on a short cover, the trade was the squeeze and i sell. if it doesn’t pop, the option lets me hold for the architecture question to resolve. which it won’t by august. the mismatch is on purpose. but i should name it so neither of us forgets which one i’m actually trading.

— brylan.

the sources: every figma-specific number on this page is grounded in figma’s own investor materials. the 2025 10-K. the Q1 2026 10-Q. the Q1 2026 earnings call and presentation. the Q4 2025 earnings call. all on figma’s investor relations page and on sec.gov. the rest. jenny wen on lenny rachitsky’s podcast. claude design on anthropic’s site. lovable, cursor, and v0 numbers from sacra. all of it is public. all of it is one search away.

disclosure: long fig via a jan 2028 $10 call. opened may 8th, 2026 at $20.04 underlying for $13.20 in premium. one contract. this is not investment advice.